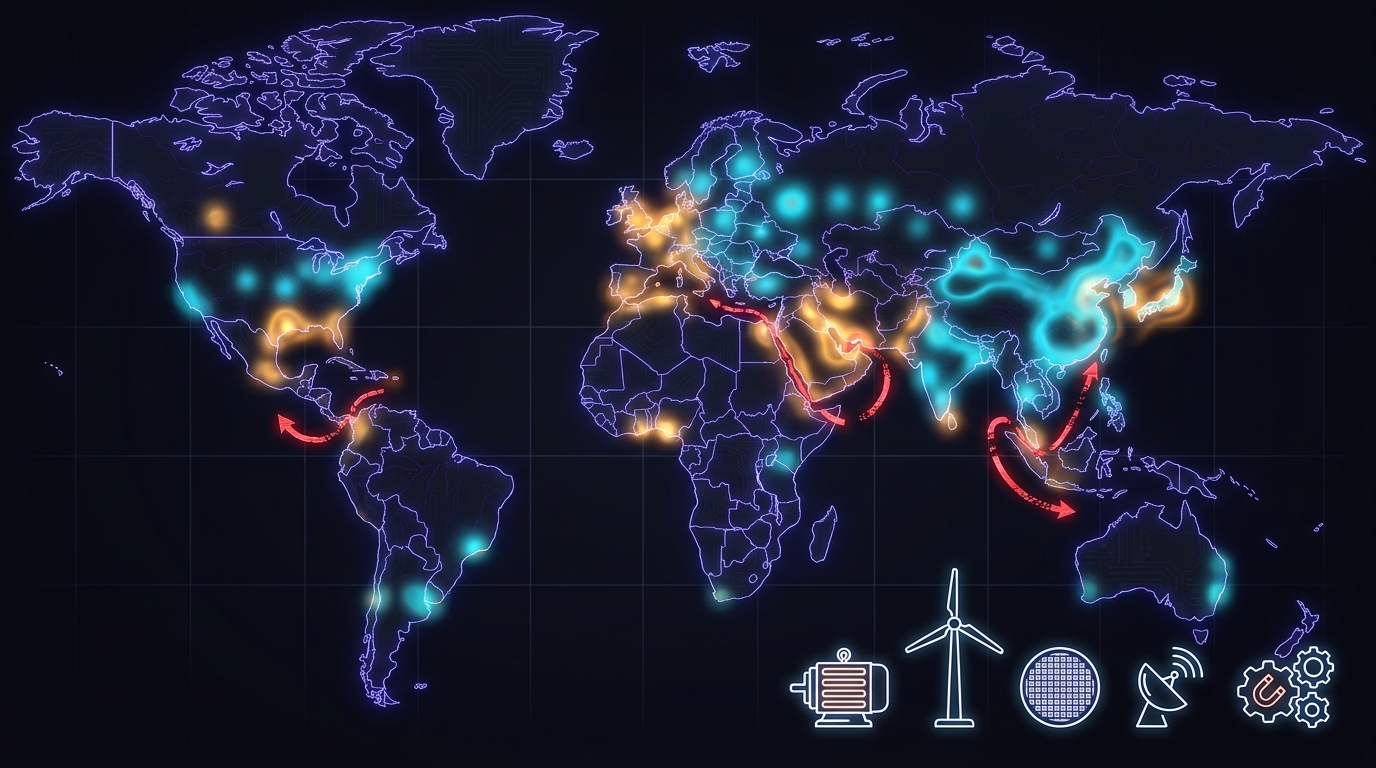

This critical minerals list is best read as a map of industrial dependence, not a scoreboard of whichever commodity is getting the most attention. The right way to sort these materials is by three pressures that show up again and again in real supply chains: how concentrated production and processing are, how hard substitution becomes once a product is qualified, and how essential the material is to magnets, batteries, semiconductors, alloys, optics, and defense hardware. That is also the cleanest answer to a common question: rare earths are a subset of critical minerals, while critical minerals is the broader policy and industry category that includes rare earth elements plus battery metals and other strategic inputs.

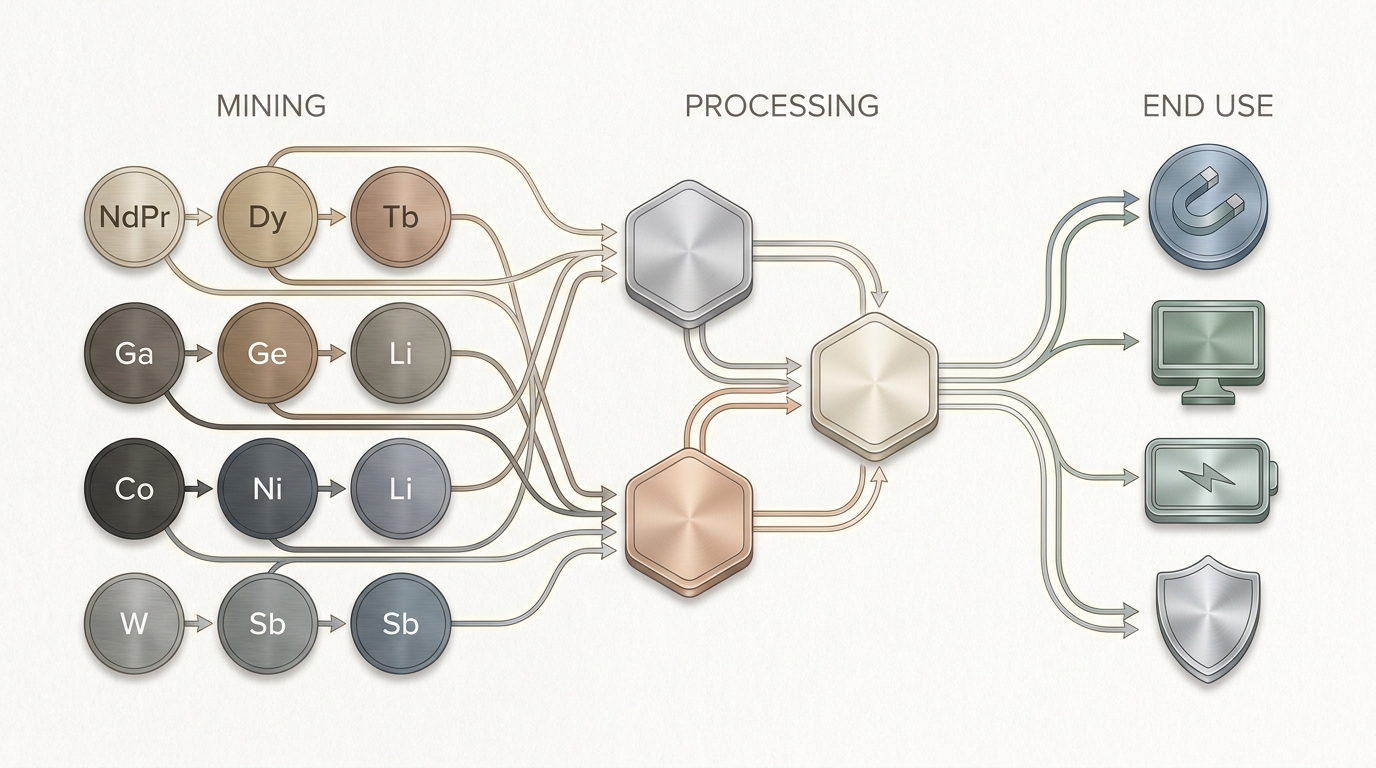

The 10 names below sit at the center of that risk map: NdPr, Dy, Tb, Ga, Ge, Li, Co, Ni, W, and Sb. Some are volume materials tied to EVs and storage. Others are tiny by tonnage but can still jam an entire procurement plan if refining capacity tightens or export controls move faster than new supply. For readers who want more detail, each entry links to a dedicated explainer, because the bottleneck is often not the orebody at all; it is the midstream step where chemistry, purity, and qualification turn a resource into something manufacturers can actually use.

1. NdPr (Neodymium-Praseodymium)

NdPr sits near the top of any serious critical minerals list because it is the workhorse input for NdFeB permanent magnets, and those magnets are embedded in EV traction motors, direct-drive wind turbines, industrial robots, precision servomotors, drones, and a long tail of defense systems. In plain terms, electrified motion leans on this material far more than casual coverage suggests. The real chokepoint is not just mining rare earth ore; it is the chain from separation to metal, alloy, and finished magnet. China still controls roughly 85% to 90% of rare earth separation and about 90% or more of NdFeB magnet manufacturing capacity, which means supply concentration is deeper in the system than many first-time readers expect. That is why NdPr belongs on the short list of strategic metals even though it is technically a rare earth product. When procurement teams assess resilience, they usually discover that “alternative supply” at the mine level does not automatically mean qualified alternative magnets at the component level. That qualification gap is where delays, redesign costs, and hidden inventory builds show up. The clean verdict: NdPr is a first-tier strategic material for anyone tracking metals for energy transition, and the signals worth watching are magnet plant buildouts outside China, separation capacity in allied jurisdictions, and whether OEMs are shifting motor designs toward lower rare-earth intensity. A deeper overview sits in this NdPr guide.

2. Dy (Dysprosium)

Dysprosium is where the rare earth story gets uncomfortable, because the metal is used in much smaller volumes than NdPr yet can be even harder to replace when high-temperature magnet performance matters. Dy is typically added in small amounts to improve coercivity and thermal stability in permanent magnets, which is why it matters for EV motors, wind applications, aerospace systems, and defense hardware expected to perform under heat and stress. The market looks small on paper, but that is exactly what makes it fragile: tiny demand does not equal easy supply when most heavy rare earth separation is still concentrated in China at levels widely estimated above 95%. Unlike a bulk metal market, dysprosium supply cannot be scaled quickly with a straightforward mine restart, because it is entangled with complex rare earth mineralogy, separation chemistry, and downstream magnet qualification. In procurement reviews, Dy exposure often hides inside a magnet contract rather than appearing as a separate line item, which means downstream buyers may not see the risk until lead times suddenly stretch. That hidden exposure is why Dy consistently ranks among the most supply-constrained names on any advanced rare earth elements list. The verdict is blunt: dysprosium is a chokepoint metal, not a volume story, and resilience improves only when buyers understand the additive chemistry inside their magnets rather than assuming all rare earth supply is interchangeable. For more technical context, see this dysprosium deep dive.

3. Tb (Terbium)

Terbium is one of the smallest markets on this list and one of the easiest to underestimate. Like dysprosium, Tb is valued for what a very small addition can do to magnet performance, especially where high coercivity is non-negotiable. It also appears in phosphors and specialized electronics, but the strategic case is really about high-spec magnets used in transport, industrial automation, and defense-adjacent systems. Supply is structurally tight because terbium occurs in low concentrations, is rarely the economic driver of a mine on its own, and depends on the same highly concentrated heavy rare earth processing chain that dominates dysprosium. In practice, that means more than 95% of refined heavy rare earth output still traces back to Chinese separation capacity. That concentration matters because even modest shifts in EV motor demand, turbine specifications, or export policy can produce outsized strain in a market this small. It is a classic chokepoint commodity: little tonnage, high leverage, and very limited room for error once an OEM has validated a magnet recipe. For retail readers building a broader view of critical metals, Tb is useful because it challenges the assumption that only large commodity markets matter. Sometimes the small additive is what stalls the system. The verdict is that terbium deserves attention precisely because it can move from obscurity to urgency very quickly, especially if magnet producers start optimizing for performance over material thrift. The companion terbium explainer goes deeper into those trade-offs.

4. Ga (Gallium)

Gallium is a textbook example of why a critical minerals list should not be built around tonnage alone. It is a low-volume material, but it sits inside high-value semiconductors such as gallium arsenide and gallium nitride that are used in RF chips, power electronics, LEDs, fast chargers, telecom equipment, radar, satellites, and military systems. The strategic role is obvious once the end uses are lined up: Ga helps modern electronics run faster, hotter, and more efficiently than silicon alone can manage in certain applications. The bottleneck is that gallium is usually recovered as a byproduct from bauxite and zinc processing, so supply does not respond cleanly to gallium demand. Even more important, China has accounted for roughly 95% to 98% of primary gallium production in recent years, giving it an extraordinary degree of leverage over a market that many downstream buyers only notice when trade restrictions arrive. That combination of byproduct dependence and geographic concentration is exactly the kind of hidden fragility procurement teams dislike. It means new supply cannot simply be willed into existence with higher prices if refining routes, feedstock access, and purification know-how are missing. The verdict: gallium is one of the most acute semiconductor-linked strategic metals, and the key indicators are export licensing, non-Chinese refining investments, and the pace of GaN adoption in power electronics. Readers wanting the fuller semiconductor angle can continue with this gallium deep dive.

5. Ge (Germanium)

Germanium rarely gets the public attention of lithium or rare earths, yet it remains one of the quietest pressure points in advanced manufacturing. Its end-use profile is unusually strategic: fiber-optic systems, infrared optics, thermal imaging, night-vision equipment, certain semiconductor applications, and some solar technologies all rely on germanium in ways that are hard to replace quickly. That makes Ge far more relevant to communications resilience and defense capability than its modest market size would suggest. Supply is constrained for a different reason than the magnet metals: germanium is typically recovered as a byproduct of zinc processing and, in some regions, from coal-related streams, so the metal’s availability is tied to other industrial decisions rather than a standalone germanium mine pipeline. China has often represented around 60% of global germanium output and an even more influential share of downstream processing, which creates the same uneasy pattern seen elsewhere in this list: specialized demand facing a concentrated midstream. In operational terms, the real risk is not just physical scarcity but specification risk. Optical and semiconductor customers do not want simply “more germanium”; they need consistent purity, reliable refining, and qualified product forms. That slows substitution and raises the cost of disruption. The verdict is that Ge belongs firmly in the upper tier of non-battery critical metals, especially for readers comparing defense-adjacent inputs with cleaner-energy names. A fuller technical overview appears in this germanium guide.

6. Li (Lithium)

Lithium is the most recognizable name on this list, but the familiar headline often hides the more useful insight: lithium is not one market, it is a chain of mine supply, brine operations, chemical conversion, and battery-grade qualification that can tighten in different places at different times. End-use demand is anchored by lithium-ion batteries for EVs, grid storage, consumer electronics, and power tools, so it is still the signature metal for electrification. Yet the bottleneck is increasingly chemical and logistical rather than purely geological. Australia, Chile, China, and Argentina account for more than 90% of global lithium mine supply, while China still handles roughly 60% of lithium chemical conversion capacity, especially in the battery-grade products the cathode industry needs. That split matters because large resources do not automatically produce reliable carbonate or hydroxide volumes at specification. Water constraints in brines, ramp-up trouble in hard-rock projects, permitting delays, and converter bottlenecks all show up before a battery maker feels truly secure. Compared with the rare earths, lithium has a broader project pipeline, but the scale of battery demand keeps it on every critical minerals list. The verdict is that lithium remains essential but increasingly nuanced: it is less of a pure scarcity story than a quality, processing, and execution story. For anyone sorting through the difference between resource abundance and usable supply, the next stop is this lithium explainer.

7. Co (Cobalt)

Cobalt’s reputation is complicated, and that is exactly why it stays on this list. It remains important in nickel-rich battery cathodes, superalloys for aerospace, catalysts, and a range of industrial applications, so the demand base is broader than the battery narrative alone. At the same time, cobalt is a supply-chain case study in concentration and governance risk. The Democratic Republic of the Congo typically provides about 70% of mined cobalt, while China controls roughly three-quarters of refining and chemical conversion, giving the market both a geographic choke point upstream and a processing choke point downstream. That structure is why cobalt can unsettle procurement teams even when battery chemistries are trying to use less of it. Lower-intensity chemistries, including LFP, have reduced cobalt demand growth in some segments, but they have not erased the metal’s role in high-performance cathodes or its continuing importance in turbine and superalloy applications. The operational lesson is that demand evolution does not automatically equal supply security. Cobalt also carries ESG baggage that can reshape contracts, audits, and sourcing strategies in a way few other battery metals do. The verdict is that cobalt is no longer the simple “must-have battery winner” story it once appeared to be, but it is still one of the most consequential strategic metals because the chain remains highly clustered and politically exposed. Readers wanting the fuller battery-versus-aerospace picture can continue to this cobalt deep dive.

8. Ni (Nickel)

Nickel is the metal on this list that most clearly forces a distinction between scale and suitability. Yes, nickel is a massive market thanks to stainless steel, but not all nickel units are equally useful for batteries. The battery story focuses on class 1 nickel and battery-grade intermediates that feed high-energy cathode chemistries, while the broader market still leans heavily on stainless demand. That split is the first reason nickel belongs in a modern critical minerals list: enormous end-use demand does not guarantee the right form of supply. The second reason is Indonesia, which has grown to roughly half of global mined nickel output and an even larger share of incremental supply growth, especially through processing routes tied to EV materials. That scale has redrawn the market. It has also introduced difficult questions around carbon intensity, permitting, waste management, and whether laterite-to-battery conversion can expand smoothly enough to meet demand without repeated operational setbacks. HPAL projects, matte conversion, and precursor qualification are not trivial steps. In procurement terms, nickel is less of a single chokepoint than gallium or terbium, but it is a major industrial dependency where processing route, specification, and ESG profile matter almost as much as headline tonnage. The verdict is that nickel is essential, but investors should treat it as a differentiated chain rather than a monolithic metal market. The finer-grained picture is laid out in this nickel explainer.

9. W (Tungsten)

Tungsten is an older industrial metal, but dismissing it as yesterday’s story would be a mistake. It remains indispensable in cemented carbides, cutting tools, drilling equipment, wear-resistant parts, aerospace components, and several defense applications where extreme hardness, density, and heat resistance are the point. That is what keeps W on any grown-up list of critical metals: the market is mature, but substitution is often poor once performance requirements get serious. China still accounts for roughly 80% or more of global tungsten mine supply and a substantial majority of downstream processing, including ammonium paratungstate and related intermediates. Outside China, supply options exist, but they tend to come with longer development timelines, smaller scale, and more exposed cost structures. This is the kind of market where a buyer may think diversification is available until they trace the chain past concentrate into chemical conversion and finished hard-metal products. Tungsten’s strategic context is therefore less about hype and more about industrial continuity. Machine shops, mining equipment, aerospace manufacturing, and defense procurement all feel the effect if tungsten units tighten or specifications narrow. The verdict is that W is a classic resilience metal: not flashy, absolutely relevant, and difficult to replace in high-performance applications. For readers comparing “energy transition metals” with defense-linked materials, tungsten is a useful reminder that the critical story is broader than batteries. More detail is available in this tungsten guide.

10. Sb (Antimony)

Antimony is probably the most under-followed material on this list, which is exactly why it deserves the final slot. It shows up in flame retardants, lead-acid battery alloys, primers and munitions, specialty glass, PET catalysts, and various chemical applications that do not always make headlines but remain deeply embedded in industrial systems. The supply chain is narrower than many expect. China has often accounted for about half of global mined antimony and a larger share of refined and chemical products such as antimony trioxide, while a meaningful portion of the remaining supply comes from a small group of jurisdictions rather than a broad, liquid global base. That creates the sort of opaque market structure where trade frictions, environmental controls, or mine disruptions can have an outsized effect. Antimony is also awkward because substitution depends heavily on the end use: in some flame-retardant systems there is room to adjust formulations, but in other applications the qualification cycle can be slow and costly. This is not a metal that benefits from abundant transparent pricing, broad producer diversity, or easy downstream flexibility. The verdict is that Sb belongs on a contemporary critical minerals list as a classic strategic holdover: smaller market, less media attention, but very real leverage in defense and industrial chemicals. Readers who want the full picture on this quietly important chokepoint can continue to the antimony deep dive.

If there is one takeaway from this critical minerals list, it is that “critical” does not simply mean geologically rare. It means a material sits inside an important technology stack and is hard to replace, slow to scale, or dangerously concentrated in a few processing hubs. For broad retail readers, the most supply-constrained names here are usually the magnet rare earths and semiconductor inputs; the largest system-level exposures are lithium, nickel, and cobalt; and the materials that often surprise newcomers are tungsten and antimony. That is also the cleanest way to separate a rare earth elements list from the broader universe of strategic metals: rare earths are one powerful subset, while the wider critical-minerals picture spans batteries, chips, optics, hard metals, and defense supply chains.