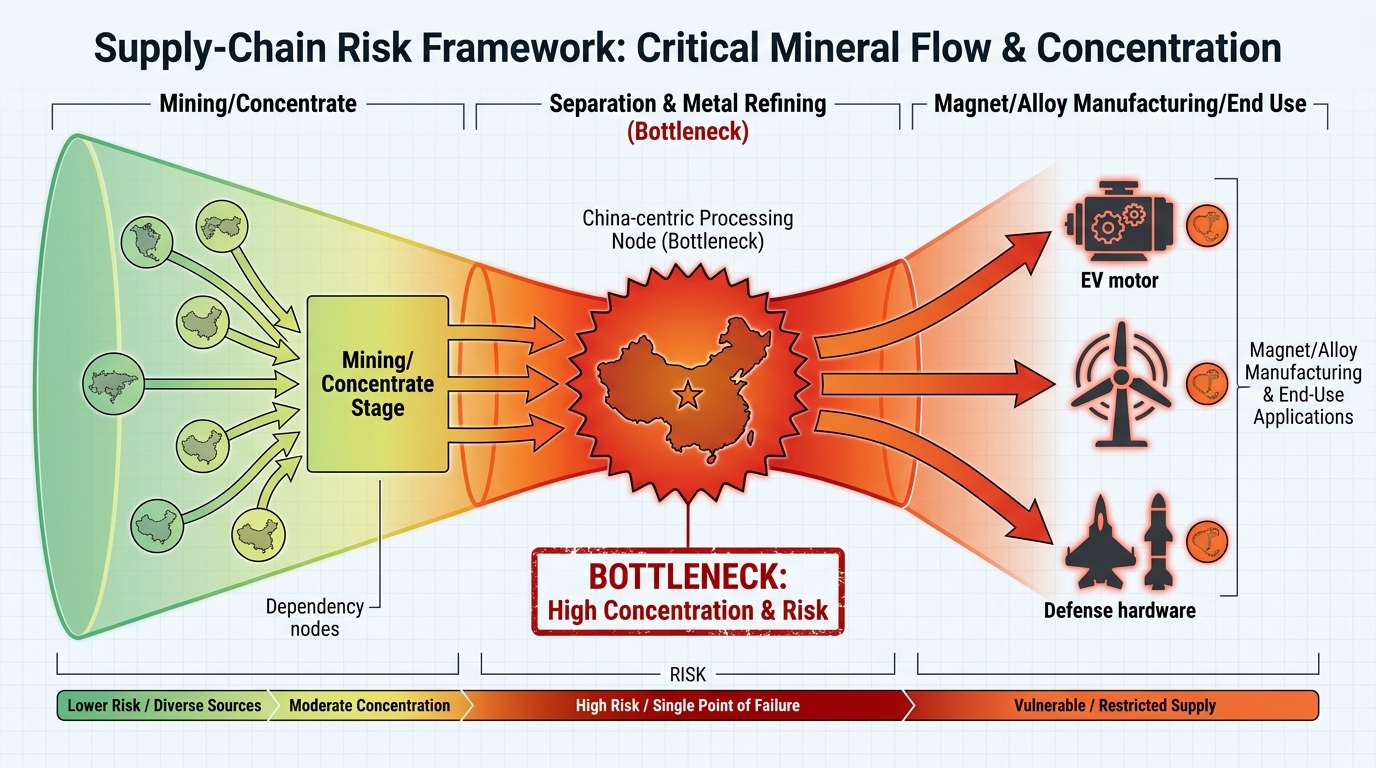

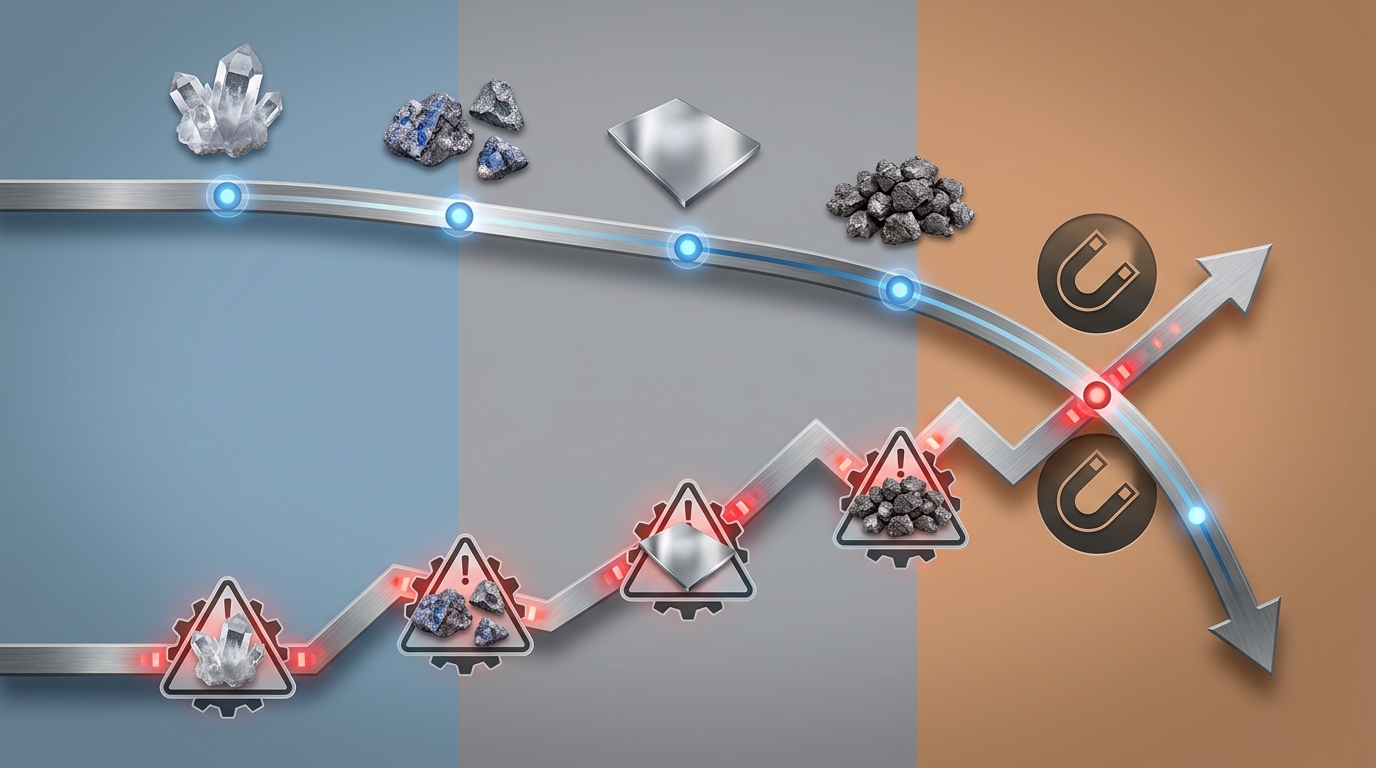

In operational reviews of rare earth suppliers, a recurring discovery moment appears early: many projects described as “rare earth production” stop at ore, concentrate, or mixed chemical product. The difficult part of the chain starts after mining. In mine to magnet terms, resilience depends on five linked stages-ore extraction, solvent extraction separation, metal reduction, alloying, and magnet manufacturing-and the main Western gaps sit in the middle and downstream steps rather than in geology alone. That distinction explains why Mountain Pass in California and Mount Weld in Western Australia matter, yet still do not by themselves create a complete non-Chinese rare earth supply chain.

- The ore extraction stage secures feedstock, but mineralogy, impurity profile, and radionuclide handling determine whether downstream rare earth processing is practical.

- Solvent extraction separation remains the central bottleneck because chemically similar rare earths require long, tightly controlled processing cascades and demanding waste-management systems.

- The metal reduction stage, NdFeB alloy strip casting, and sintered magnet production introduce yield, contamination, and qualification risks that many front-end mining narratives understate.

- China dominates each stage not only through capacity, but through integration, operating experience, equipment ecosystems, and qualification history with end users.

- Observed non-Chinese resilience patterns include partial vertical integration, alternate processing routes, staged qualification of intermediates, and selective redesign to reduce heavy rare earth dependence.

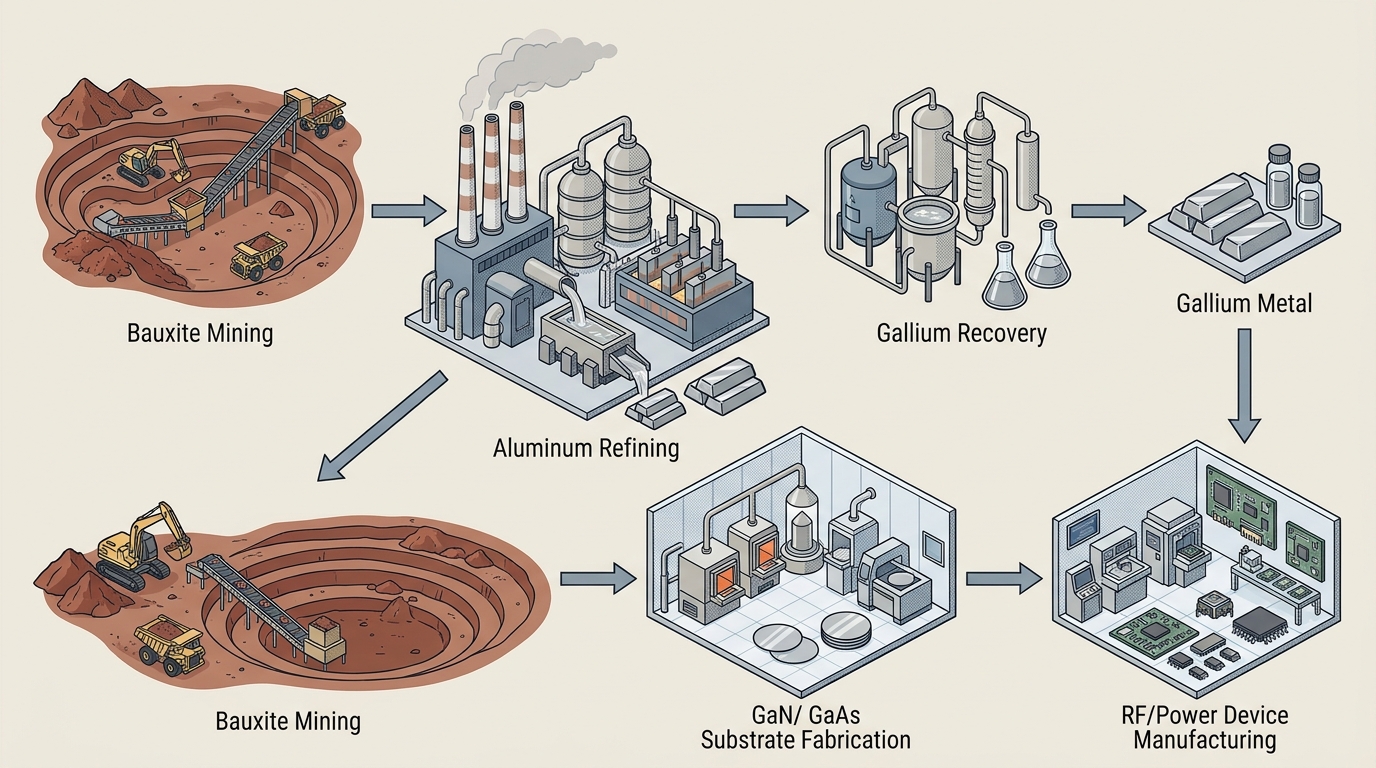

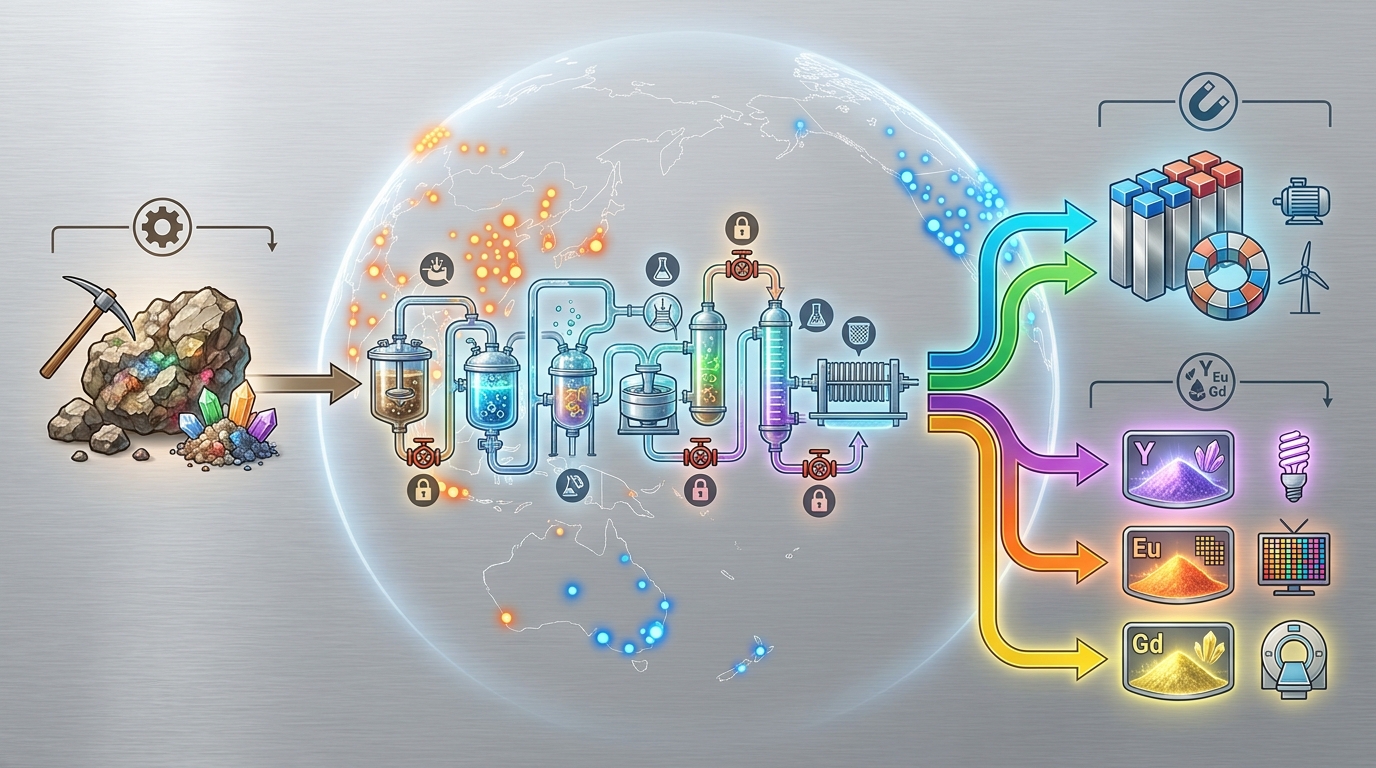

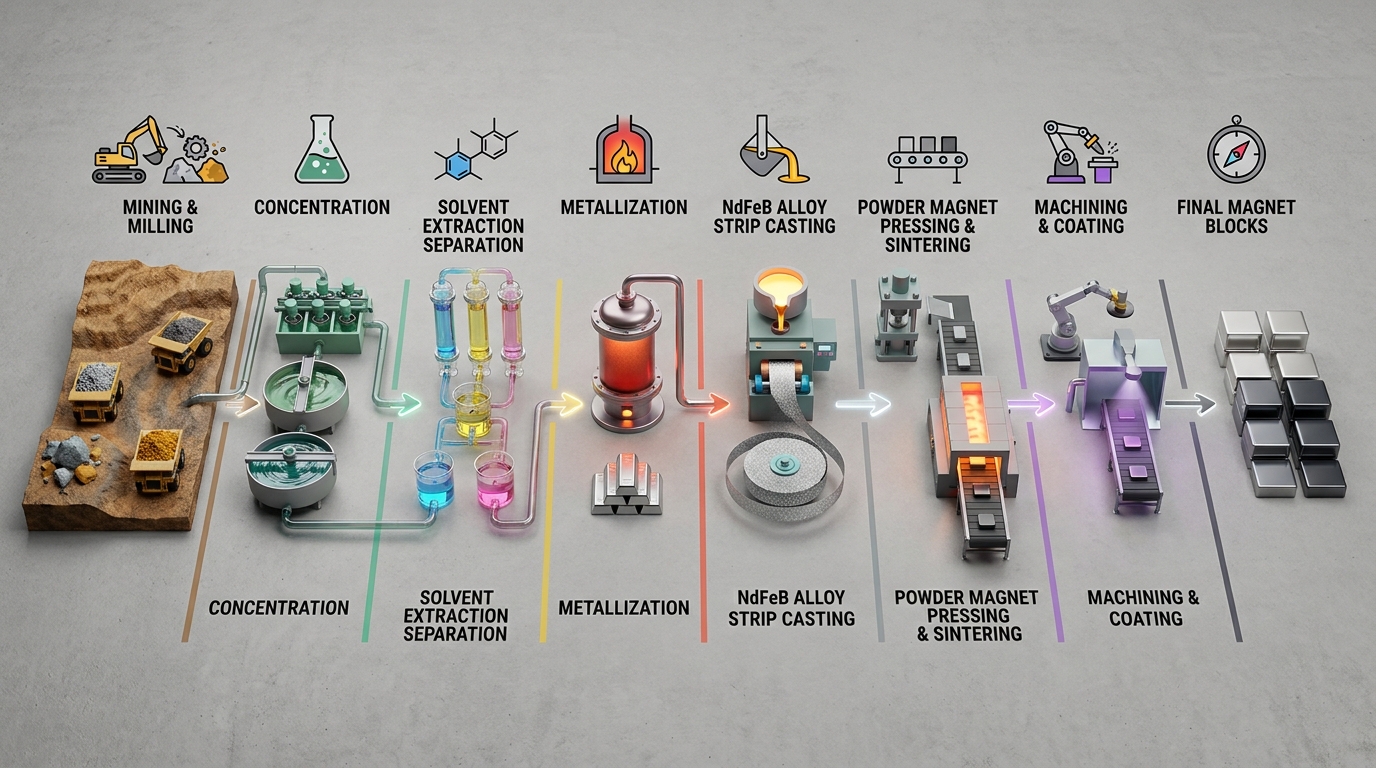

What mine to magnet actually covers

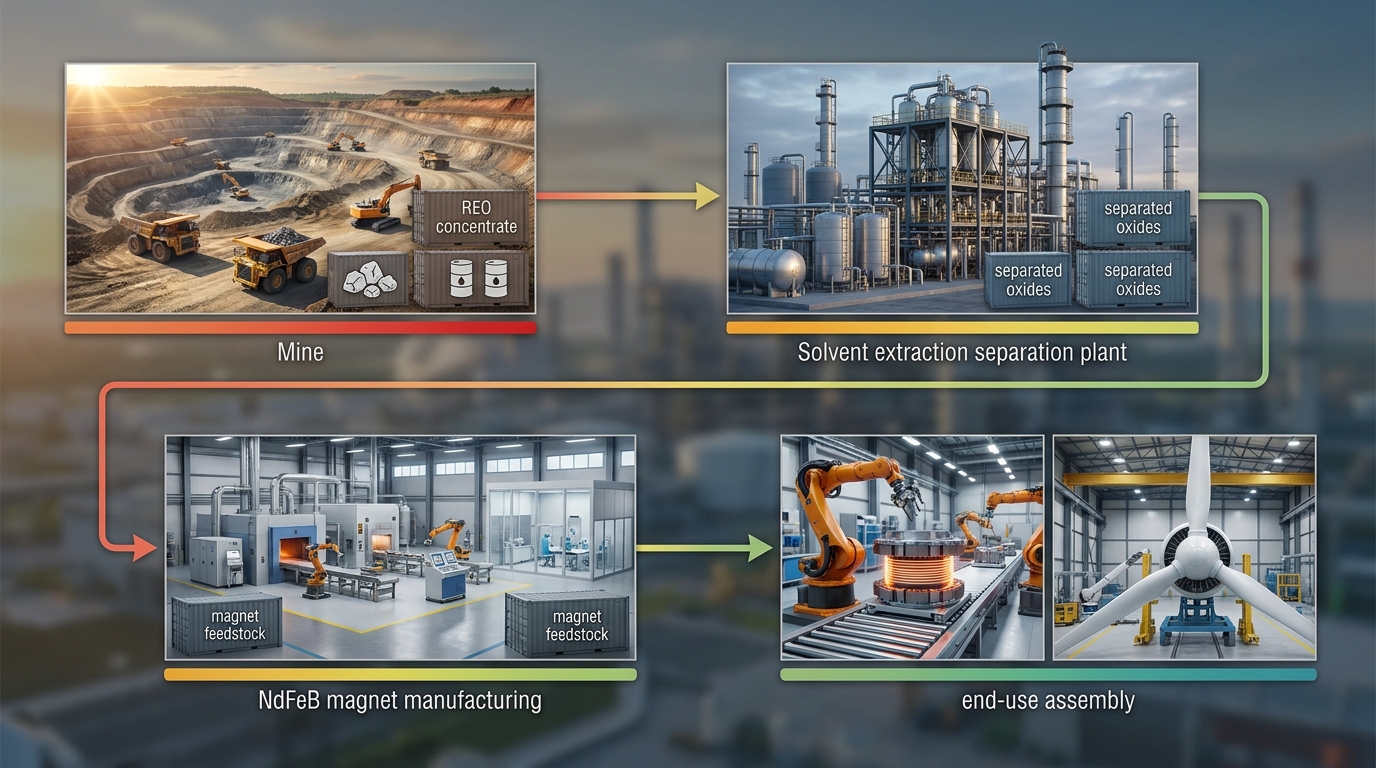

Mine to magnet is shorthand for a full rare earth value chain that turns mined material into finished permanent magnets, usually NdFeB products for motors, actuators, sensors, and high-performance industrial systems. In analytical terms, the chain is only complete when material moves through five distinct industrial transformations. Ore is extracted and beneficiated; mixed rare earths are separated into individual oxides or refined streams; oxides are reduced into metal; metal is alloyed into magnet feedstock; and that feedstock is turned into finished magnets through powder processing, pressing, sintering, machining, coating, and magnetization.

A second discovery moment often follows from that definition: a country can host an active rare earth mine and still remain dependent on foreign processing at several points. That is the central structural issue in western rare earth discussions. Front-end capacity exists in several jurisdictions, but broad commercial depth across all five stages remains limited outside China.

Stage 1: Ore extraction and concentrate production

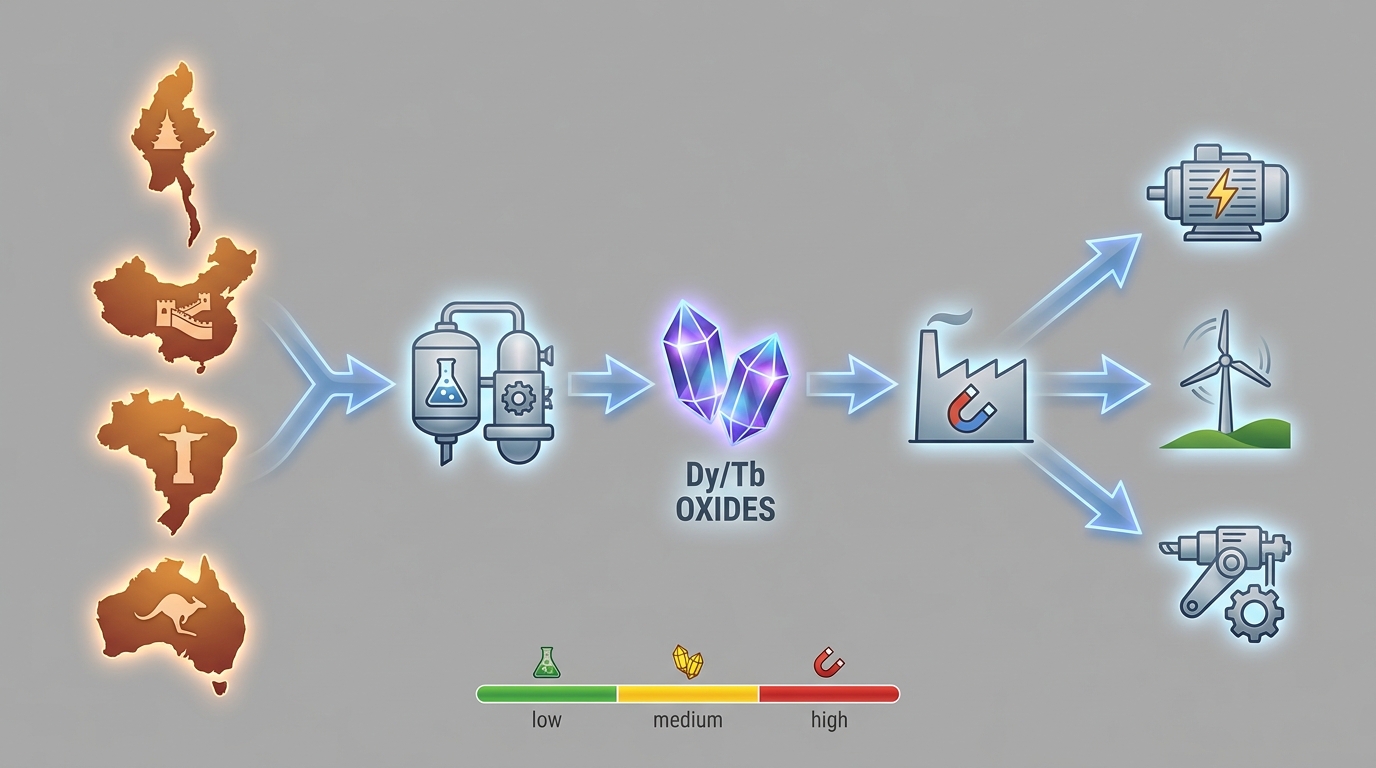

The ore extraction stage is the most visible part of the rare earth supply chain, but it is not the hardest to localize. Mountain Pass, California, remains the best-known active U.S. rare earth mine and a key Western source of ore and concentrate. Mount Weld, Western Australia, remains one of the highest-profile non-Chinese rare earth feedstock sources and is linked to Lynas’s downstream processing chain. Smaller or emerging projects exist in Canada, Sweden, Greenland, Brazil, and parts of Africa, although most are not yet integrated into a full mine-to-magnet route.

Analytically, the useful question at this stage is not simply whether ore exists, but whether the ore can move cleanly into downstream chemistry. TREO, or total rare earth oxides, is only one part of that picture. Mineralogy determines liberation behavior, concentrate quality, and how readily the mixed rare earth stream can be processed later. Bastnaesite, monazite, xenotime, and ionic clay systems create different operational profiles. Waste streams also matter: thorium, uranium, and other regulated impurities can move a project from straightforward mining into complex compliance management under U.S., Australian, or European permitting regimes.

Observed failure modes at the mining stage include unstable concentrate specification, overreliance on headline TREO without downstream recoverability evidence, and underestimation of residue handling where radioactive impurities are present. In practice, two projects with similar grade language can create very different downstream outcomes once impurity suite and mineralogy are examined closely.

Stage 2: Solvent extraction separation

Solvent extraction separation is often the least understood step in rare earth processing and the most important bottleneck in the chain. Rare earths are not exceptionally rare in geological terms; the difficulty lies in separating chemically similar elements through repeated extraction, scrubbing, and stripping stages. This is a plant-scale chemical operation with tight process control, sensitive reagent balance, and a heavy documentation burden around waste, emissions, and water treatment.

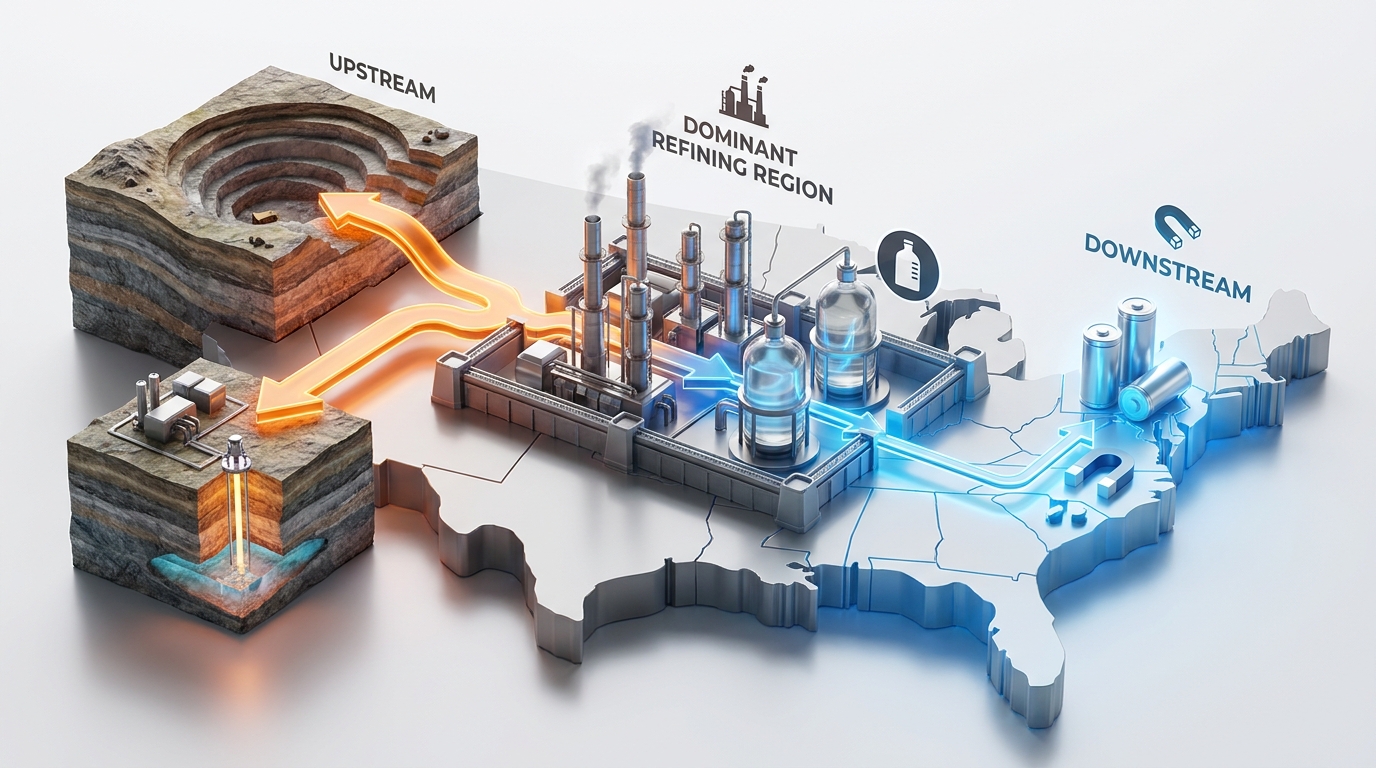

China dominates this stage because it spent decades building integrated separation systems, operator know-how, reagent supply, and waste-treatment infrastructure. The Western position is narrower. Australia-linked production associated with Mount Weld and Lynas is one of the most visible non-Chinese channels. The United States has mining capability and has treated separation as a strategic build-out area, but the overall commercial base remains much smaller than China’s. In practical terms, a mine without reliable separation access remains exposed, even if ore production itself is strong.

Common failure modes here include feed variability that destabilizes the extraction circuit, impurity carryover that affects downstream oxide specification, and delays linked to environmental controls rather than core chemistry alone. Commissioning risk is also unusually high: nameplate concepts often look linear on paper, while real plant tuning depends on many campaigns of operating data.

Stage 3: Metal reduction and metallization

The metal reduction stage is where separated oxides become usable rare earth metal. This step receives less public attention than mining or magnets, yet it is one of the sharpest industrial cliffs in the mine to magnet pathway. Rare earth metals are reactive, oxygen-sensitive, and demanding to handle. Purity is not a cosmetic issue: ppm-scale contamination can echo into alloy performance and magnet qualification later in the chain.

Western rare earth capacity is comparatively thin at this point. The challenge is structural. Metallization depends on reliable separated oxide supply, specialized equipment, and a downstream customer base that can absorb metal or alloy at consistent specification. China benefits from proximity between oxide producers, metal makers, alloy plants, and magnet manufacturers. That integration reduces logistics friction and creates faster feedback when purity or yield drifts.

Observed failure modes include oxidation during handling, inconsistent metal purity, and process economics that weaken when metallization sits far from both oxide production and alloy consumption. A recurrent discovery moment in supplier diligence is that a technically credible oxide producer may still have no practical bridge into stable metal production.

Stage 4: Alloying and NdFeB alloy strip casting

After metallization, rare earth metal is combined with iron, boron, and selected additives to make magnet alloy feedstock. For NdFeB systems, NdFeB alloy strip casting is a critical step because it shapes microstructure, oxidation behavior, and later powder characteristics. In operational terms, this is where chemistry starts to merge with materials engineering: a cast alloy that looks acceptable in bulk form can still create powder behavior that destabilizes pressing, sintering, or final magnetic performance.

China’s dominance at this stage reflects cluster effects as much as capacity. Alloying sits next to metal supply on one side and magnet manufacturing on the other. That allows rapid correction when composition drifts, heavy rare earth loading changes, or customer specification tightens. Western capacity exists in narrower form, but it is less deeply networked, and that matters because alloying is highly sensitive to upstream purity and downstream qualification.

Typical failure modes include microstructural inconsistency, oxygen pickup, and dependence on a single upstream metal route. Where dysprosium or terbium enters the design, exposure to heavy rare earth availability adds another layer of risk inside the rare earth supply chain.

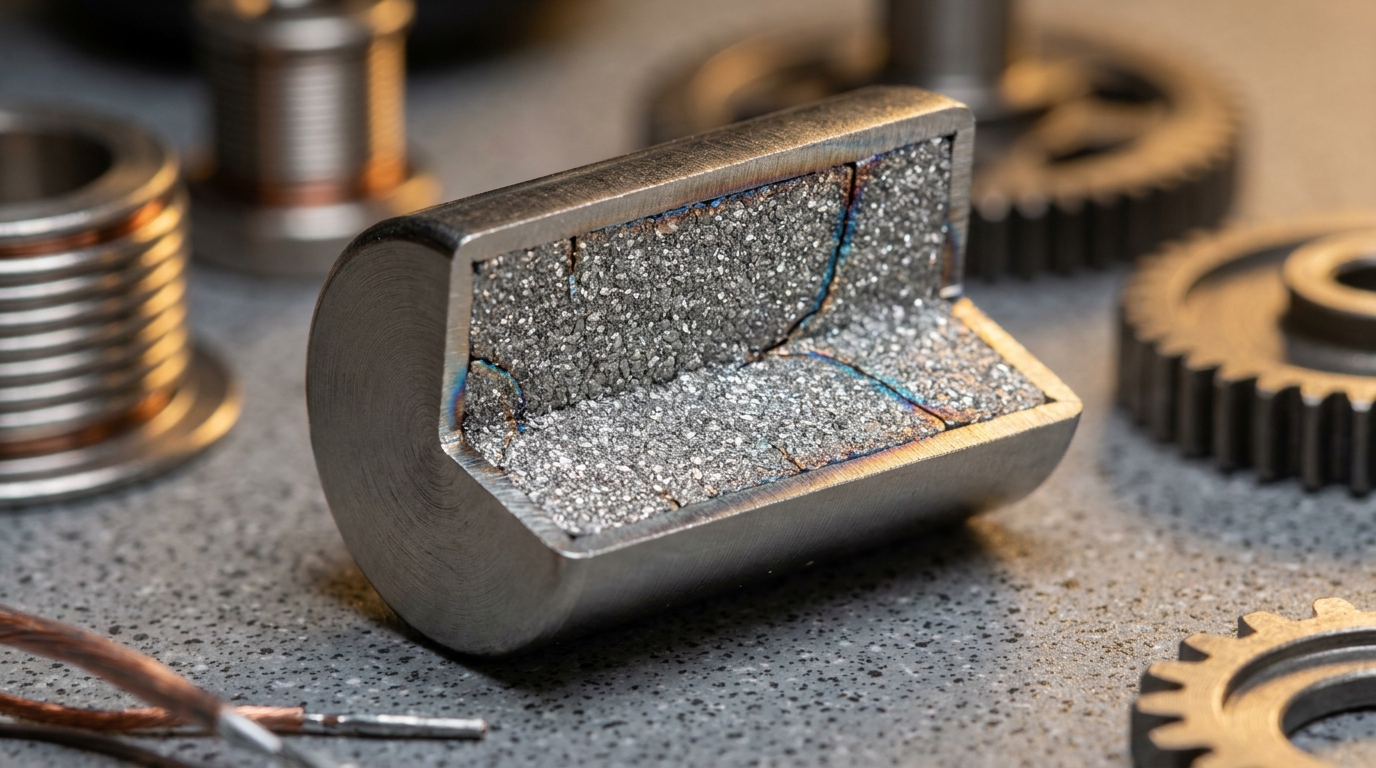

Stage 5: Sintered magnet production

Sintered magnet production is the last industrial transformation and often the hardest to stand up at scale. Powder is milled, aligned, compacted, sintered, machined, coated, and magnetized into finished product. Performance depends on more than chemistry alone. Press behavior, grain boundary control, thermal profile, corrosion resistance, machining yield, and coating adhesion all influence whether a magnet can enter automotive, aerospace, defense, robotics, or industrial motor service.

China dominates this stage through installed manufacturing base, specialized tooling, coating ecosystems, and qualification history with end users. Western rare earth efforts have increasingly focused on restoring magnet-making capability, but qualification remains a major barrier. Magnet customers often assess not only elemental composition, but route history: oxide source, metal purity, powder characteristics, sintering behavior, and consistency across production lots. That means a factory can exist before a dependable commercial magnet stream fully exists.

Observed failure modes include insufficient lot-to-lot consistency, coating failures in end-use environments, and weak integration between alloy specification and finished magnet requirements. At this final stage, the value chain stops behaving like commodity processing and starts behaving like a qualified advanced-manufacturing system.

Cross-stage evidence used in risk mapping

- Orebody mineralogy, TREO distribution, and the split between light and heavy rare earth content.

- Impurity profile, including thorium or uranium-bearing residues and the jurisdiction-specific compliance pathway for handling them.

- Flowsheet maturity for solvent extraction separation, including sensitivity to feed variability and waste-treatment integration.

- Metal purity evidence, oxygen-control practices, and traceability from oxide to reduced metal.

- Alloy reproducibility, especially around NdFeB strip casting, powder behavior, and heavy rare earth additions.

- Qualification status for sintered magnet production, including documentation, product consistency, and end-use acceptance history.

Observed resilience patterns outside China

Several non-Chinese approaches appear repeatedly across the western rare earth landscape. One pattern is partial vertical integration around a mine and one or two downstream stages rather than the whole chain at once. Another is geographic splitting of stages, where ore originates in one jurisdiction and later processing takes place elsewhere under tighter compliance control. A third pattern is qualification of intermediate products-mixed carbonate, separated oxide, alloy, or magnet—rather than immediate pursuit of end-to-end internalization. Redesign to reduce heavy rare earth intensity also appears in some applications, although substitution at system level remains constrained by performance requirements.

These patterns clarify the larger point. The difficulty in standing up western rare earth production is not the absence of rock. It is the absence of a broad, connected industrial chain with chemical separation depth, metallization capability, alloying experience, and magnet qualification history comparable to China’s. In mine to magnet analysis, the middle stages usually determine whether front-end mining becomes strategic capacity or remains only a feedstock source.