In day-to-day manufacturing reviews, neodymium rarely appears first as a polished metal sample. It usually appears as NdPr oxide feed availability, metal conversion capacity, magnet grade qualification, and thermal requirements inside a traction motor or wind generator. That operating context explains why the question “what is neodymium” is wider than a chemistry definition. In industrial terms, neodymium is the rare earth element best known for enabling high-performance permanent magnets, and its importance comes from the chain around it: separated oxides, refined metal, alloy production, finished NdFeB magnet output, and then the motor, generator, sensor, or actuator that turns material science into usable force.

- Commercial relevance usually sits in NdPr oxide, metal conversion, and NdFeB magnet manufacturing rather than in pure neodymium metal alone.

- A common point of confusion is the difference between NdPr oxide, neodymium metal, and the finished neodymium magnet; each sits at a different supply-chain stage.

- EV traction motors and direct-drive wind turbines concentrate demand because they value compact, high-torque permanent magnets.

- Observed failure modes often come from downstream bottlenecks such as separation, metal-making, heavy rare earth additions, and magnet qualification rather than from mine output alone.

What neodymium is in industrial terms

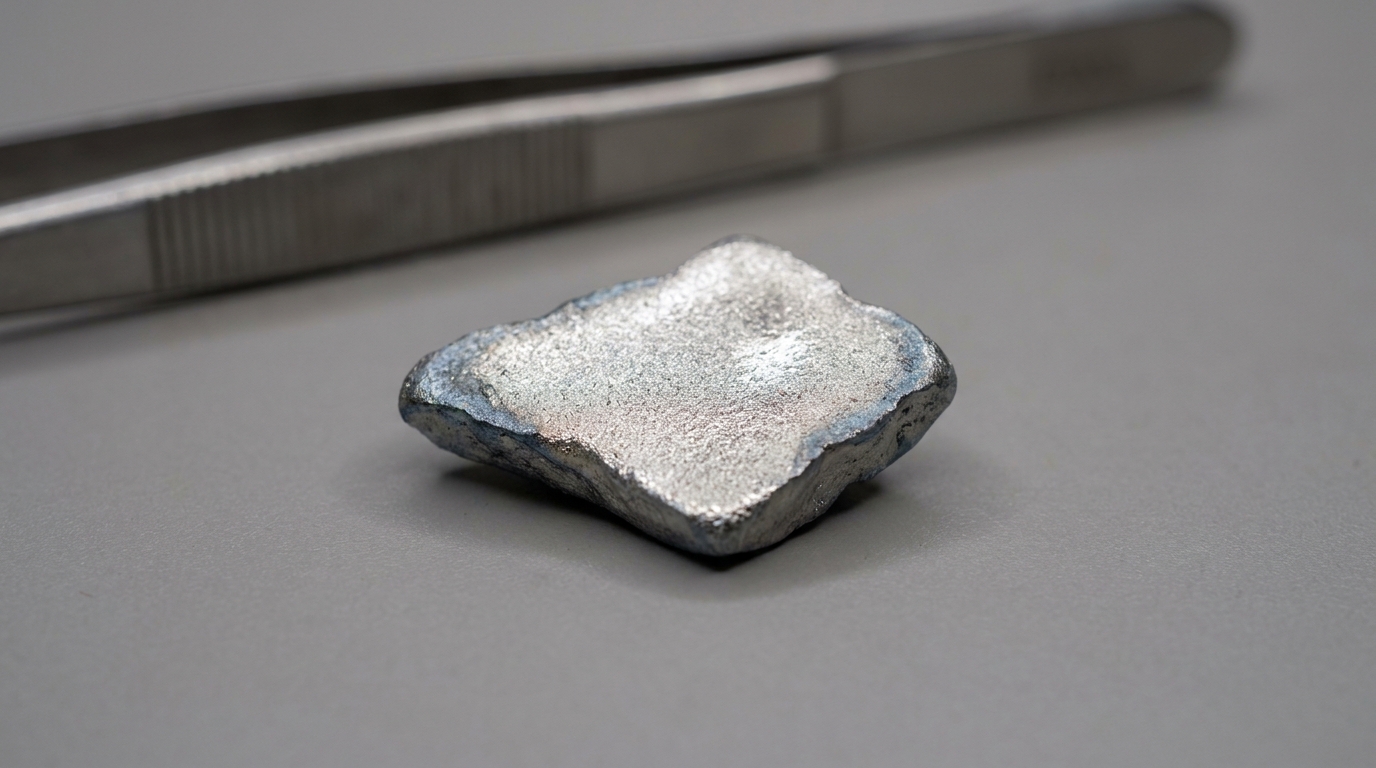

Neodymium, symbol Nd and atomic number 60, is a lanthanide rare earth element. In physical terms it is a soft, silvery metal, but that description only captures a small part of its commercial role. The industrial significance of neodymium comes from magnet performance. When combined with iron and boron in the NdFeB system, it helps create the strongest widely used permanent magnets in modern manufacturing.

A recurring discovery in supply-chain discussions is that “rare earth availability” and “magnet availability” are not the same thing. Ore bodies may be described in TREO, or total rare earth oxides, yet a high TREO figure does not automatically translate into a strong neodymium or praseodymium output profile. Another discovery is that neodymium is often discussed as a stand-alone metal even though many commercial transactions and plant configurations are organized around intermediates and alloys rather than around pure metal inventories.

Where the commercial value sits: NdPr oxide, metal, and finished magnets

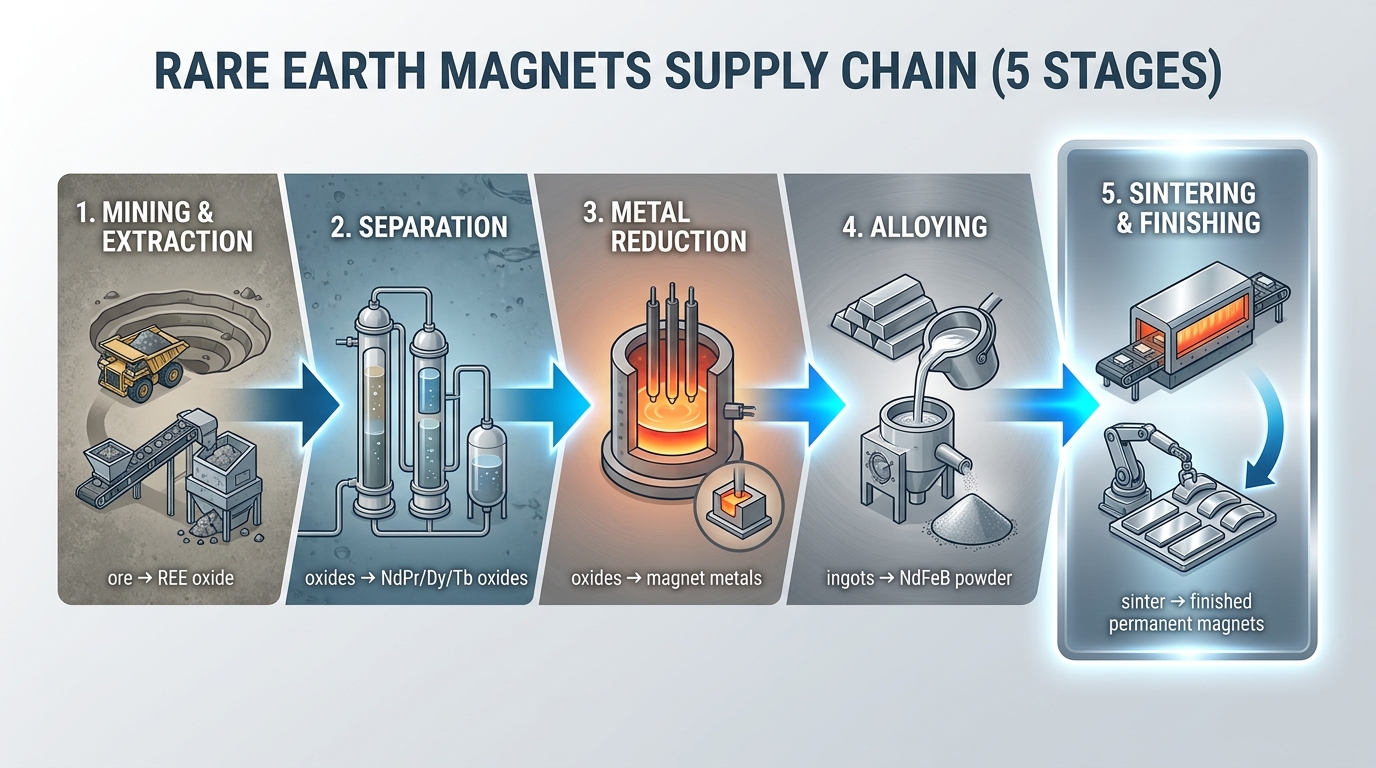

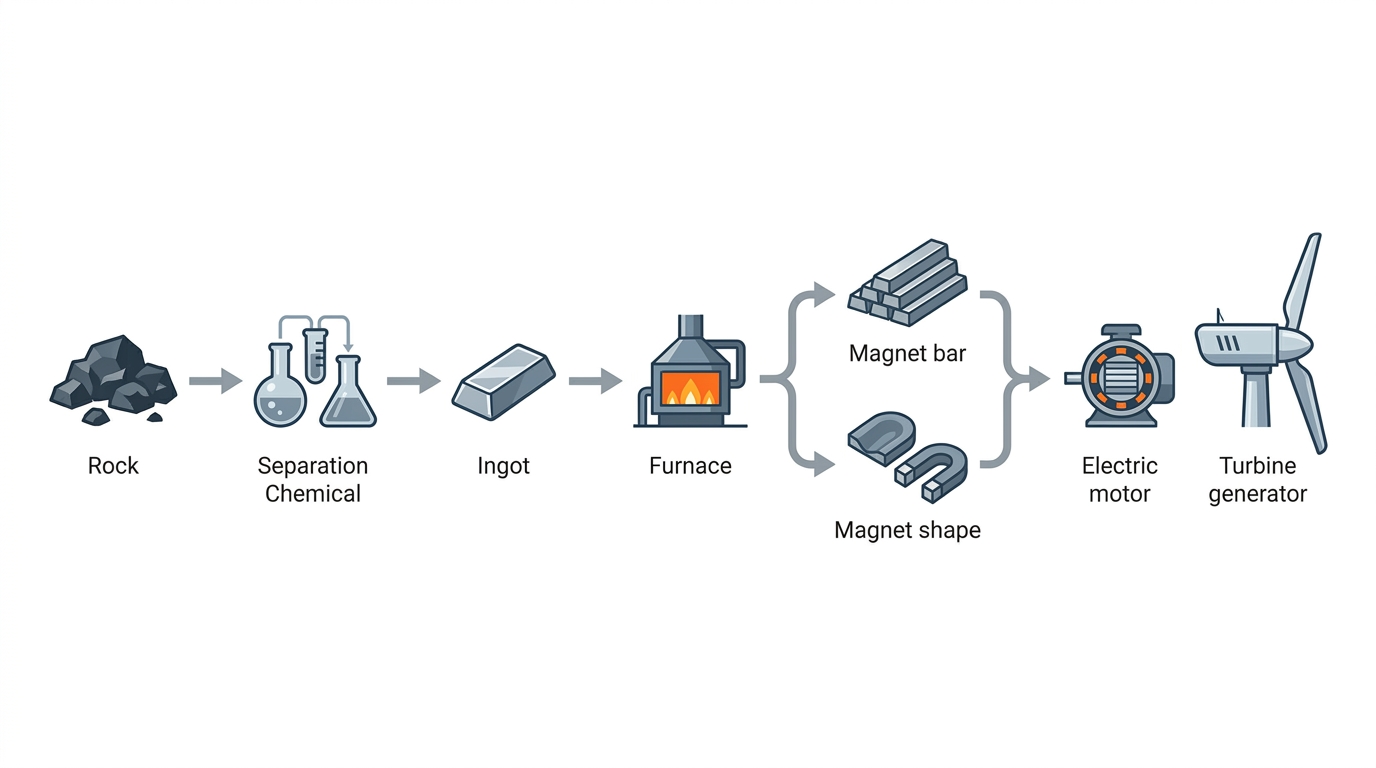

For most readers asking what is neodymium, the most useful clarification is that the supply chain has several distinct material forms.

- NdPr oxide is the separated rare earth oxide stream that usually contains neodymium and praseodymium together. In practical market terms, this is the main feedstock used in magnet supply chains.

- Neodymium metal is the refined metal form used in downstream alloying and specialty applications. It sits further along the chain and reflects metallization capability, not just mine or separation output.

- NdFeB magnets are the finished magnetic materials made from neodymium, iron, and boron, often with small additions of dysprosium or terbium in higher-temperature grades.

This distinction matters because a disruption at one stage does not always appear at another stage immediately. An operation can have mine output and still lack separated NdPr oxide. Another operation can have oxide but lack metal conversion or alloying capacity. A motor producer can have access to magnets yet remain exposed to a narrow set of qualified grades or coatings. In practice, the phrase “neodymium supply” often compresses several bottlenecks into one label, even though the stress point may sit in separation chemistry, metallization, or magnet finishing.

NdFeB magnet basics: why a neodymium magnet is not just “a strong magnet”

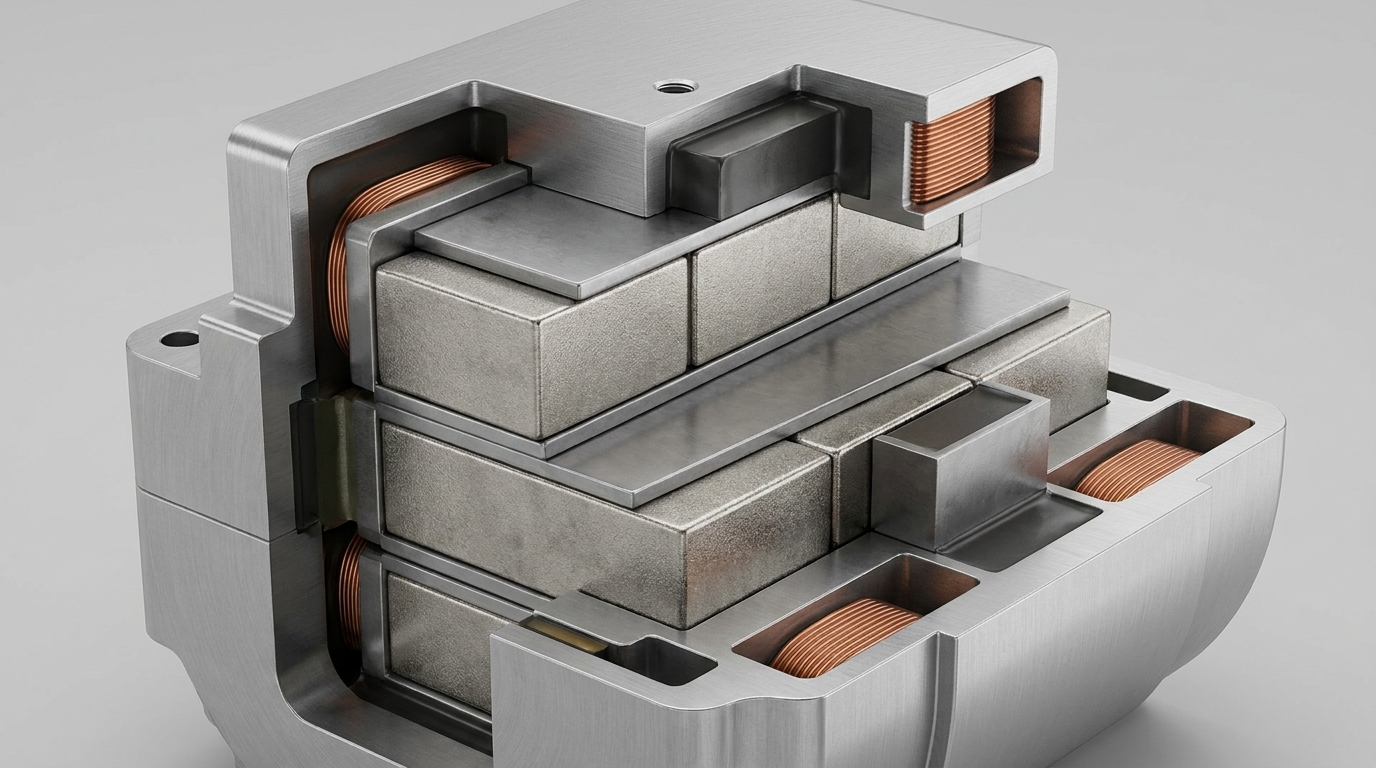

The standard industrial magnet family here is NdFeB, short for neodymium-iron-boron. The magnetic phase is commonly associated with Nd2Fe14B, which gives the material its very high magnetic strength relative to size. That strength-to-volume advantage is the reason a neodymium magnet has become central in compact motors, actuators, speakers, robotics, and automation systems.

Two production routes dominate commercial discussions.

- Sintered NdFeB is produced through powder metallurgy. It generally delivers the highest magnetic performance and is the form most closely associated with demanding applications such as EV traction motors and many permanent-magnet generator designs.

- Bonded NdFeB mixes magnetic powder with a polymer binder and shapes it by molding or similar routes. It is useful where design flexibility and complex geometries matter, but its magnetic performance is usually lower than sintered material.

That sintered-versus-bonded distinction is important because public discussion often treats all neodymium magnets as interchangeable. In real industrial use, they are not. A bonded magnet used in a compact sensor or automotive auxiliary system does not solve the same engineering problem as a sintered magnet in a high-performance traction motor. The end-use sector so shapes the relevant supply-chain risk: powder characteristics, thermal behavior, coating quality, and high-temperature rare earth additions can matter as much as raw oxide availability.

Neodymium uses: from electronics to heavy industrial systems

The simplest answer to “what is neodymium used for?” is that it is used primarily in permanent magnets. Those magnets then appear across a very wide range of products. Common neodymium uses include speakers, headphones, hard disk drives, power tools, industrial servomotors, pumps, sensors, actuators, robotics, automation equipment, EV traction motors, and wind turbine generators.

The scale shift now attracting the most attention comes from electrified transport and renewables. Earlier consumer electronics demand was spread across many small units. EVs and wind, by contrast, concentrate magnet demand into large industrial systems where qualification standards, traceability, thermal margins, and manufacturing consistency become more visible. That is one reason public industrial policy in jurisdictions such as the United States, the European Union, Japan, South Korea, and Australia increasingly treats magnets as a strategic manufacturing input rather than as a niche specialty material.

Why neodymium is so closely linked to EVs

The phrase neodymium EV appears so often because many electric vehicles use permanent-magnet motors that value compact size, torque density, and efficiency. In those architectures, NdFeB magnets allow a motor to deliver strong performance in a limited package envelope. That matters in passenger vehicles where mass, space, thermal control, and drive efficiency all interact with vehicle design.

General industry observations often place rare earth content for an EV traction motor in a range from hundreds of grams to a few kilograms, depending on motor architecture, vehicle size, and whether the platform uses one motor or multiple motors. That is not a universal number. Some EVs use induction or other magnet-light architectures, and magnet formulations can vary depending on praseodymium balance and the use of dysprosium or terbium in higher-temperature grades. Still, the broad pattern is clear: EV demand links neodymium not just to the motor itself, but to a chain of oxide separation, metal conversion, alloying, sintering, machining, coating, and final motor assembly.

Another recurring discovery is that the phrase “neodymium magnets are in every EV” overstates the case. They are in many EVs, not all EVs. The reason that distinction matters is analytical rather than semantic. A market with several motor architectures behaves differently from a market with only one dominant architecture. Substitution exists, but performance trade-offs and redesign burdens also exist, which is why magnet demand remains structurally important even when alternative motor choices are available.

Wind demand and the special role of direct-drive turbines

Wind power is the other major demand pillar. Here the central distinction is between geared turbines and direct-drive turbines. Direct-drive designs typically rely more heavily on permanent magnets because they eliminate the gearbox and use a large generator operating at lower rotational speeds. In practical terms, that makes direct-drive installations far more relevant to neodymium demand than a simple count of turbines alone would suggest.

Public technical discussion varies on exact material intensity because turbine rating, generator design, and supplier choices differ. What remains consistent is the structural effect: direct-drive wind can create large, concentrated orders for magnet material. That concentration changes how demand is felt across the chain. A consumer-electronics market spreads usage across many small units, while a wind program can pull material through alloying and magnet capacity in large project waves.

Structural supply context: where the real bottlenecks tend to appear

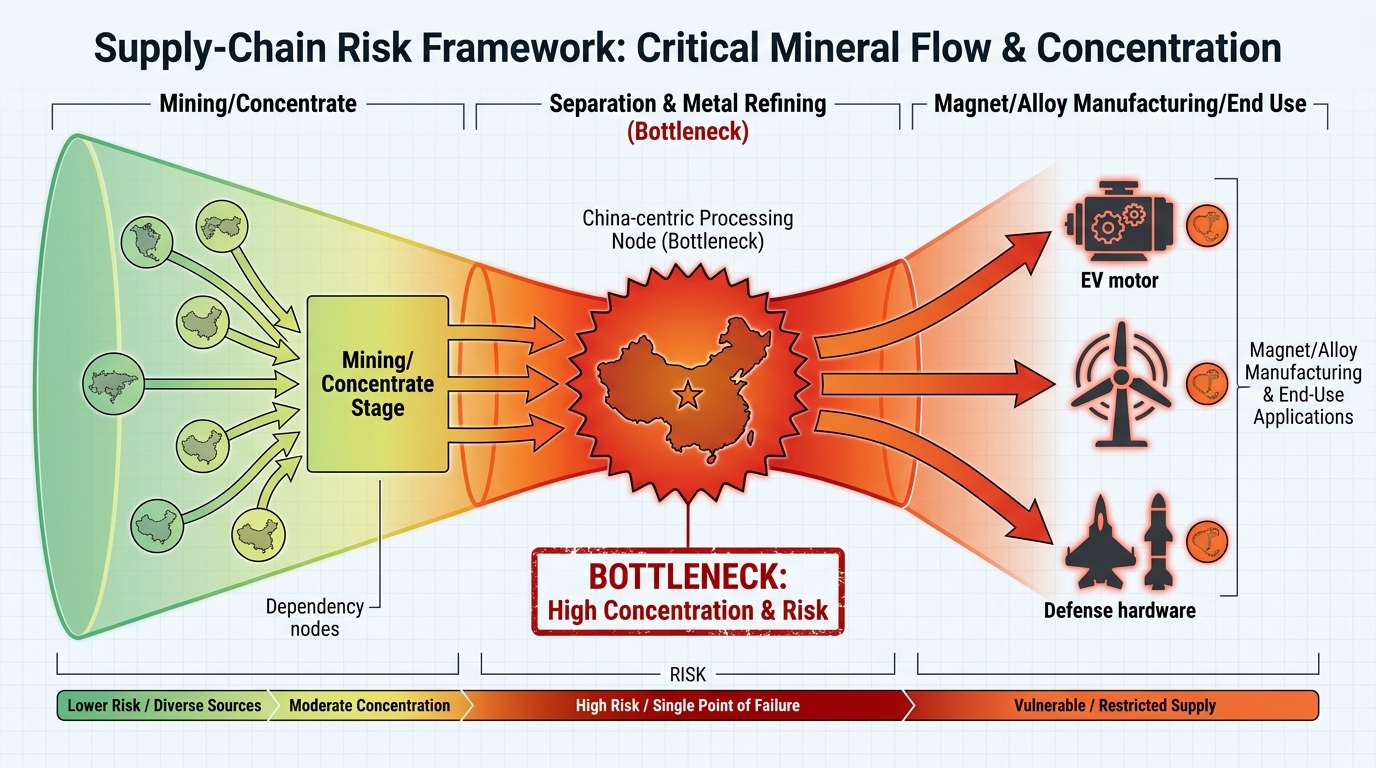

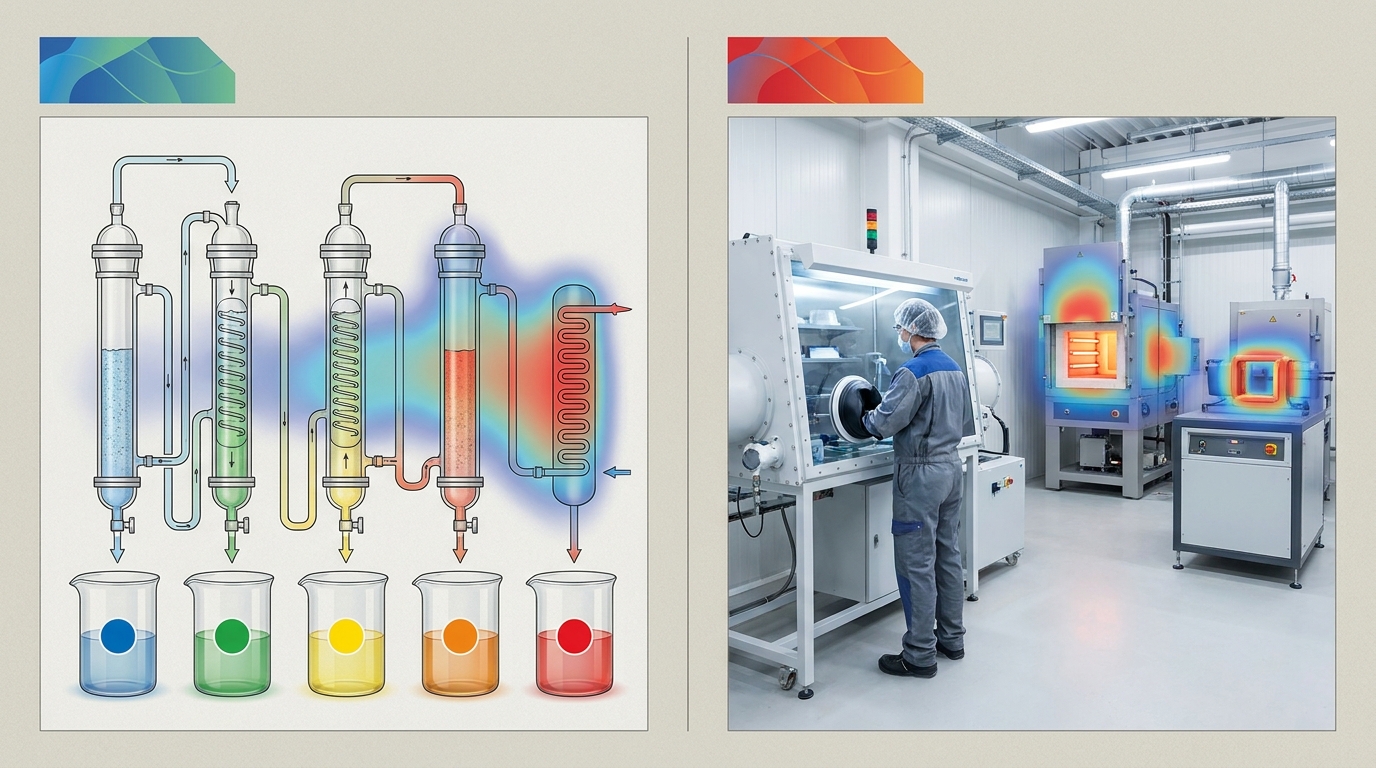

Neodymium supply risk is often described as a mining story, but in practice it is a processing and manufacturing story as well. The full chain usually includes mining, concentration, cracking and leaching, solvent extraction and separation, NdPr oxide production, metal-making, alloying, magnet manufacturing, and then integration into motors or generators. Each stage has its own technical barriers and qualification demands.

A frequent public-market observation is the geographic concentration of downstream capability. Mining and concentrate production exist across several jurisdictions, including China, Australia, and the United States. However, separation, metal conversion, alloying, and magnet production have historically remained far more concentrated, especially in China. Japan also retains long-standing materials and magnet expertise, while Europe and North America are major end-demand regions in automotive and energy equipment. One trade pattern that appears repeatedly in public disclosures is material leaving one jurisdiction as concentrate or intermediate, passing through East Asian processing and magnet ecosystems, and then returning to Western manufacturing bases as finished magnet material or integrated components.

That structure creates several recognizable failure modes. One is the assumption that diversified mine supply automatically equals diversified magnet supply. Another is the belief that oxide availability resolves all downstream exposure, when metallization, high-purity alloy control, sintering, machining, coating, and grade qualification may still be concentrated. A further complication comes from dysprosium and terbium, which are often added to some high-temperature NdFeB grades. In that setting, the neodymium story is not only about neodymium; it is also about access to heavy rare earth inputs that help magnets retain performance under higher thermal loads.

Recycling adds a second structural theme. End-of-life magnets from electronics, industrial equipment, EVs, and wind systems represent a potential secondary source, and public discussion increasingly treats recycling as part of long-term supply resilience. Yet recycling has its own constraints: collection, disassembly, contamination control, and processing routes all determine whether magnet scrap becomes reusable feedstock. The operational lesson is that recycling is highly relevant, but it does not erase the complexity of the primary chain.

Questions that often surface in neodymium coverage

What is neodymium used for?

Neodymium is used mainly in permanent magnets, especially NdFeB magnets, which then go into motors, generators, sensors, audio equipment, robotics, automation systems, and many compact high-performance devices. Its commercial importance comes from magnetic performance rather than from broad use of the pure metal by itself.

Why are neodymium magnets in every EV?

That phrasing is too broad. Neodymium magnets are in many EVs, not every EV. Where they are used, the logic is straightforward: permanent-magnet motors offer strong torque density and efficient packaging. Where they are not used, an alternative motor architecture usually reflects a different engineering trade-off rather than an absence of demand for high-performance motors.

How much neodymium does a wind turbine use?

There is no single number that fits all turbines. Material intensity depends heavily on turbine rating and generator design. The most important analytical distinction is whether the turbine uses a direct-drive permanent-magnet system. Direct-drive designs generally make wind far more relevant to neodymium demand than geared designs do.

In one sentence, neodymium is a rare earth element whose industrial value comes mainly from enabling NdFeB magnets, and those magnets now sit at the center of many EV, wind, automation, and electronics supply chains. That is why the simplest definition of what is neodymium quickly becomes a broader explanation of processing stages, magnet forms, demand concentration, and manufacturing dependencies.