Securing Rare Earth Supply: Strategic Playbook for Business Leaders

Why this matters: As electric vehicles, wind turbines, robotics, and defense systems proliferate, securing neodymium, praseodymium, dysprosium, and terbium becomes a board‐level mandate. Price spikes from $80 to $200/kg in under six months (Fastmarkets, 2026) and shifting export quotas (China Mof, 2025) show that supply shocks can erode margins, delay product launches, and trigger stakeholder backlash.

Executive Summary

Business leaders face two intertwined risks in rare earths: cost volatility and supply concentration. This guide translates technical points into tangible actions—mapping exposure, structuring contracts, diversifying sources, and building midstream partnerships—to protect EBITDA, preserve launch schedules, and maintain competitive advantage.

1. Business Objectives: Defining Success

Your north star is secure access at acceptable cost and acceptable risk. Success for industrial buyers and investors looks like:

Production continuity: Zero unplanned shutdowns due to magnet shortages.

Margin stability: Reducing input‐cost variance by 50% versus benchmark indices.

Negotiation leverage: 10–15% better pricing through multi‐year indexed contracts.

Example: A European wind‐turbine OEM secured a five‐year NdPr contract with a floor/ceiling pricing formula, cutting cost spikes by 40% in 2026 (internal client data).

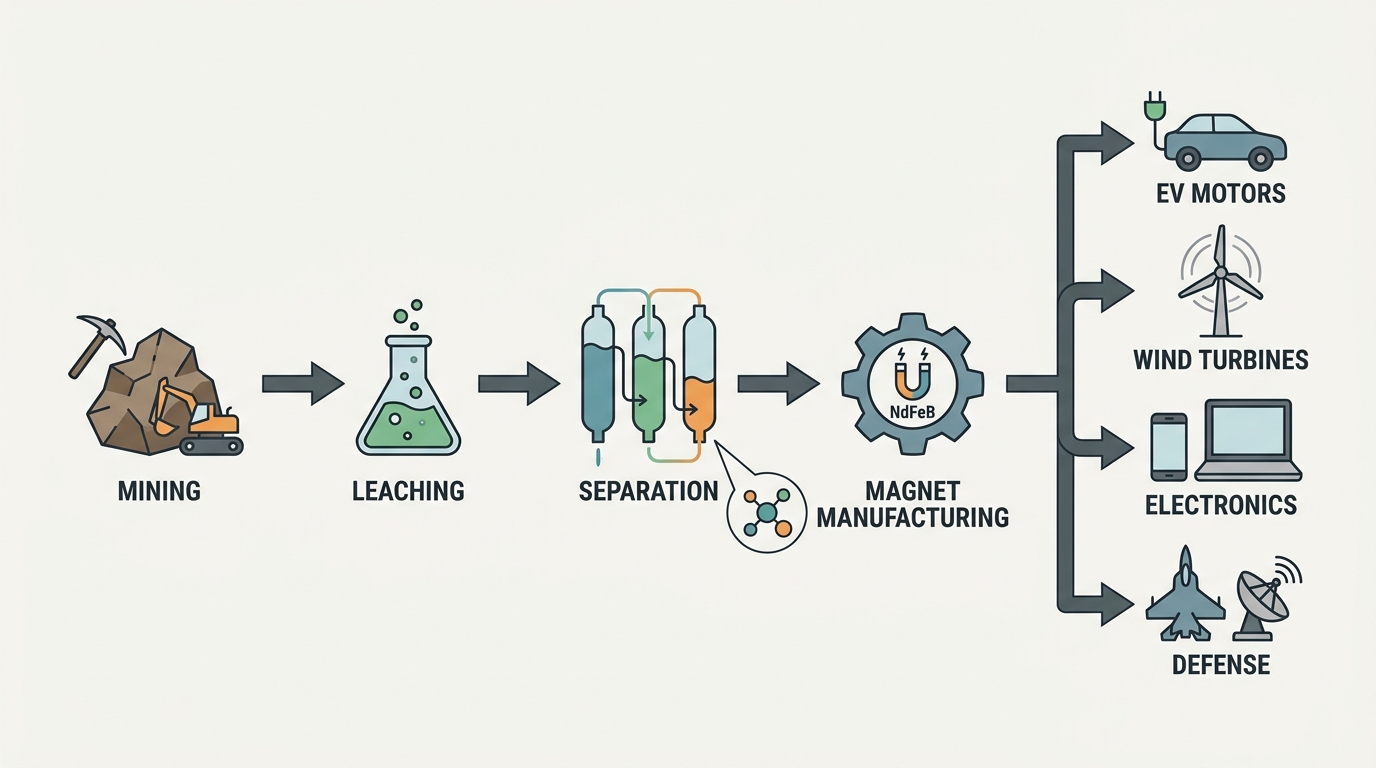

Illustrate the rare-earth refining and separation bottlenecks

2. Investment Overview: Balancing Cost, Time & Resources

Building resilience is a multi‐year commitment. Allocate resources across three horizons:

Short‐term (0–6 months): Supply‐chain mapping, benchmark subscriptions, and contract review. Estimated budget: $50K–$150K for market intelligence and legal fees.

Medium‐term (6–18 months): Dual‐source qualification, test batches, ESG audits, and safety‐stock build‐up. Example investment: $1–2M yields 3–4 months of cover for key magnets.

Long‐term (18–60 months): Equity stakes or offtake in separation, recycling, or magnet plants. A 5% stake in a midstream partner can unlock priority allocations and 0.5–1% EBIT uplift annually.

Industry outlooks project 15% annual growth in magnet demand through 2030 (BloombergNEF, 2024). Yet non‐China capacity remains under 20% of total (Lynas ~10%, MP Materials ramping; industry estimate, 2024).

3. Implementation Roadmap

Map Exposure: Identify every product and supplier that uses NdPr, Dy, Tb or their alloys. Build a tier‐three supplier register with geographies and lead times.

Build Market Visibility: Track Shanghai Metals Market and Fastmarkets benchmarks, China quota announcements (20–30% swings), and U.S. Defense Logistics stockpile levels.

Create Supply Optionality: Qualify at least two non‐China suppliers for each critical material. Negotiate indexed pricing clauses with caps/floors and allocation rights.

Strengthen Midstream: Partner in separation, recycling, or magnet assembly. Establish memoranda of understanding (MOUs) with timelines and performance milestones.

Case in point: An automotive OEM reduced project delays by 20% after co‐investing in a U.S. recycling pilot, securing 10% of its 2028 NdPr needs at fixed fees.

4. Risk Mitigation: Common Pitfalls

All rare earths are not the same: Report NdPr, dysprosium, and terbium separately—light vs. heavy elements carry different bottlenecks and price dynamics.

Mine capacity ≠ usable supply: Verify separation, alloy, and magnet‐making capacity plus customer qualification status.

Overreliance on China: Build regional alternatives in Australia, North America, or Southeast Asia and scenario‐test quota reductions.

ESG oversights: Include environmental, social, and waste‐handling diligence—shutdowns often begin with regulatory or community pushback.

Average pricing traps: Use trigger‐based governance: NdPr spikes above planning bands or quota cuts should auto‐escalate to finance and procurement heads.

5. Success Metrics & Dashboard

Measure leading indicators, not just spend:

Supply visibility: % of rare earth exposure mapped through tier‐two and tier‐three suppliers.

Diversification: % of NdPr, Dy, Tb from qualified non‐China sources.

Inventory resilience: Months of cover for magnet‐critical materials.

Contract quality: % of spend under multi‐year agreements with clear pricing formulas and force majeure terms.

Lead‐time stability: Variance in magnet/component lead times versus plan.

ESG traceability: Audit completion rate and remediation actions.

Circularity: Recycled or recovered material share.

Example dashboard trigger: NdPr > $160/kg for 10 consecutive days → invokes emergency procurement review.

6. Partner Selection: Criteria for Success

End-to-end expertise: From ore to magnet, with deep understanding of bottlenecks at each step.

Market intelligence: Real-time tracking of pricing, quotas, ramp-ups, and demand proxies like EV production.

ESG & regulatory competence: Expertise in radioactive residue, permitting, and traceability requirements.

Global reach: Regional insight across China, Australia, Southeast Asia, North America, and Europe.

Board-level communication: Translating complexity into actionable capital allocation and risk‐management decisions.

Red flag: Advisors promising a “quick exit” from China or treating mine ownership as a complete strategy.

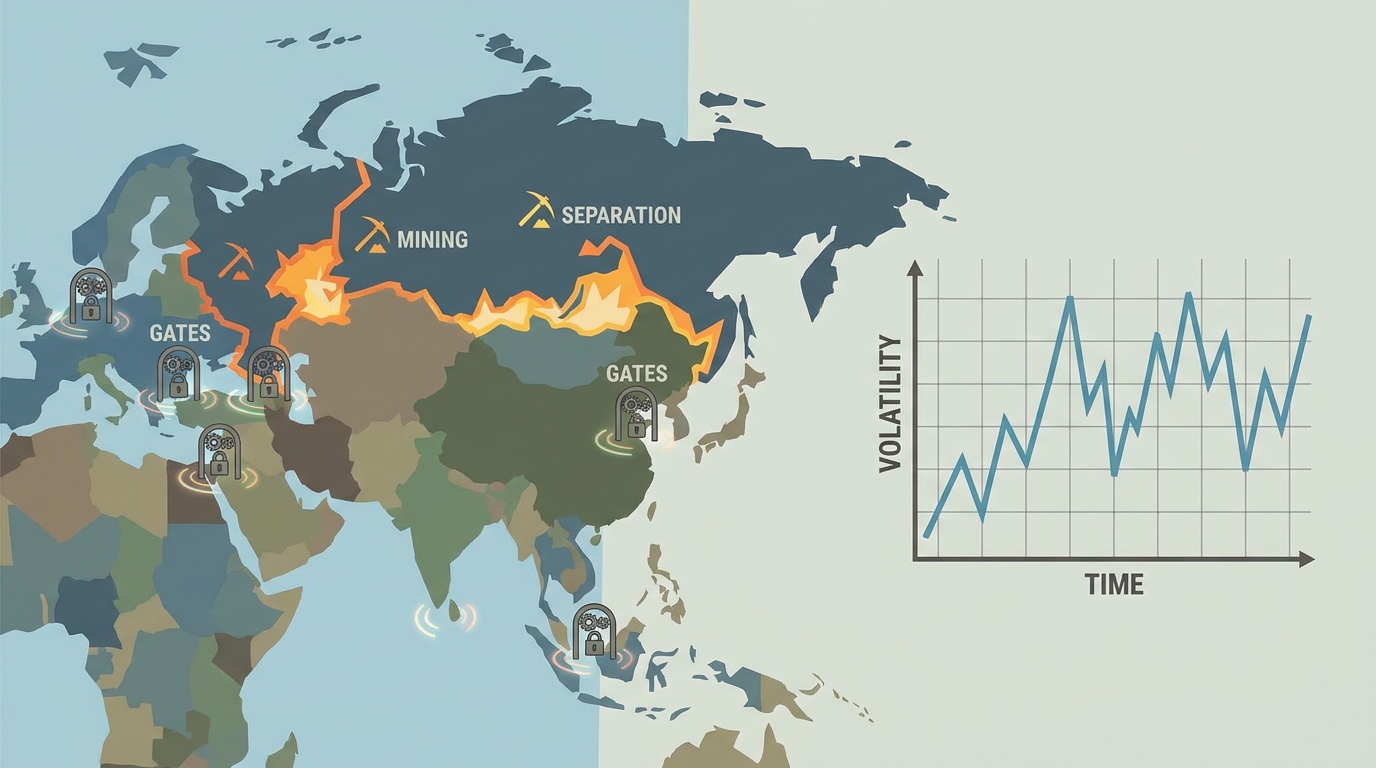

Communicate concentration risk and price volatility signals

Conclusion & Next Steps

Rare earth materials are strategically valuable because separation, refining, and magnet production remain concentrated and complex. Business leaders win by treating rare earths as a continuity‐of‐supply ecosystem, not a simple commodity play. Prioritize visibility, diversify suppliers, structure robust contracts, invest in midstream optionality, and monitor triggers to act before shortages hit the P&L.

Why this guide? Physical strategic metals can play a role in portfolio diversification, treasury protection, or supply assurance, but the business risk sits in the details of custody, documentation, and exit planning. This guide is written for investors, family offices, procurement teams, and physical commodity buyers who need to evaluate physical strategic metals storage at an oversight level. Estimated review time: about 8 minutes.

Executive Overview

Price is only part of the decision. In physical metals, value is shaped by purity, provenance, storage quality, insurance, and how easily a buyer will accept the metal later.

Buy from recognized sources. For bullion, favor LBMA-accredited or equivalent refiners and well-established dealers with transparent pricing, published buyback terms, and a credible operating history.

Choose units that support liquidity. For gold and silver, 1 oz to 100g bars often provide a practical balance between value density and resale flexibility. Larger bars can suit larger mandates but may narrow the buyer pool.

Documentation is part of the asset. Hallmarks, serial numbers, invoices, assay certificates, and chain-of-custody records directly affect resale confidence and compliance readiness.

Segregated, insured, audited storage is usually the institutional default. It improves title clarity and reduces counterparty uncertainty compared with unallocated or informal arrangements.

Not all strategic metals are equally liquid. Gold and silver generally have broad resale markets, while platinum, palladium, nickel, cobalt, lithium-related materials, and specialty alloys may require specialized channels and tighter specifications.

What This Means for You: If your organization cannot quickly answer what it owns, where it is stored, how purity was verified, who insures it, and how fast it can be sold or transferred, the program is not yet institutional-grade.

1. Business Objective

Success in a physical metals program is not simply “owning metal.” Success means holding material that is verifiable, properly titled, securely stored, and realistically resellable under normal market conditions. The right objective depends on whether the buyer is acting as an investor, a family office, or a procurement function securing future supply.

For investors and family offices: the goal is capital preservation discipline, clean provenance, and orderly access to liquidity.

For procurement teams: the goal is dependable specification, inventory integrity, and reduced supply-chain disruption.

For all buyers: the goal is to avoid hidden carrying costs, custody disputes, or resale discounts caused by incomplete documentation or unsuitable storage.

A strong business objective can be stated simply: hold physical metal in a form and jurisdiction that preserves authenticity, protects ownership rights, and supports an efficient exit when needed.

What This Means for You: Treat physical metal as an operating asset with governance requirements, not just as a purchase. Oversight should cover title, control, auditability, and exit readiness from day one.

2. Investment Overview

The total cost of ownership for physical metal includes more than the purchase price. Leaders should approve a full lifecycle budget that covers acquisition, verification, storage, insurance, transport, legal review, and periodic audit or resale testing.

Time commitment: a new program typically takes several weeks to structure, approve counterparties, open custody arrangements, and finalize documentation standards.

Capital outlay: budget for spot price plus dealer premium, logistics, assay or verification costs where needed, storage fees, and insurance.

Internal resources: treasury or investment leadership, procurement, legal, compliance, tax, and finance should all have a defined role.

Policy decisions: decide early on acceptable metal types, approved refiners, target jurisdictions, storage model, insurance rules, and exit channels.

For bullion, well-known refiners and mints such as those operating to internationally recognized standards can simplify future resale. For industrial or battery-linked strategic metals, the cost structure may also include sampling, laboratory testing, packaging controls, and specialist logistics.

What This Means for You: The most expensive mistake is often not overpaying on day one; it is discovering during a sale, audit, or dispute that the asset was never configured for smooth ownership and transfer.

Segregated depository vault setup and custody controls (illustrative).

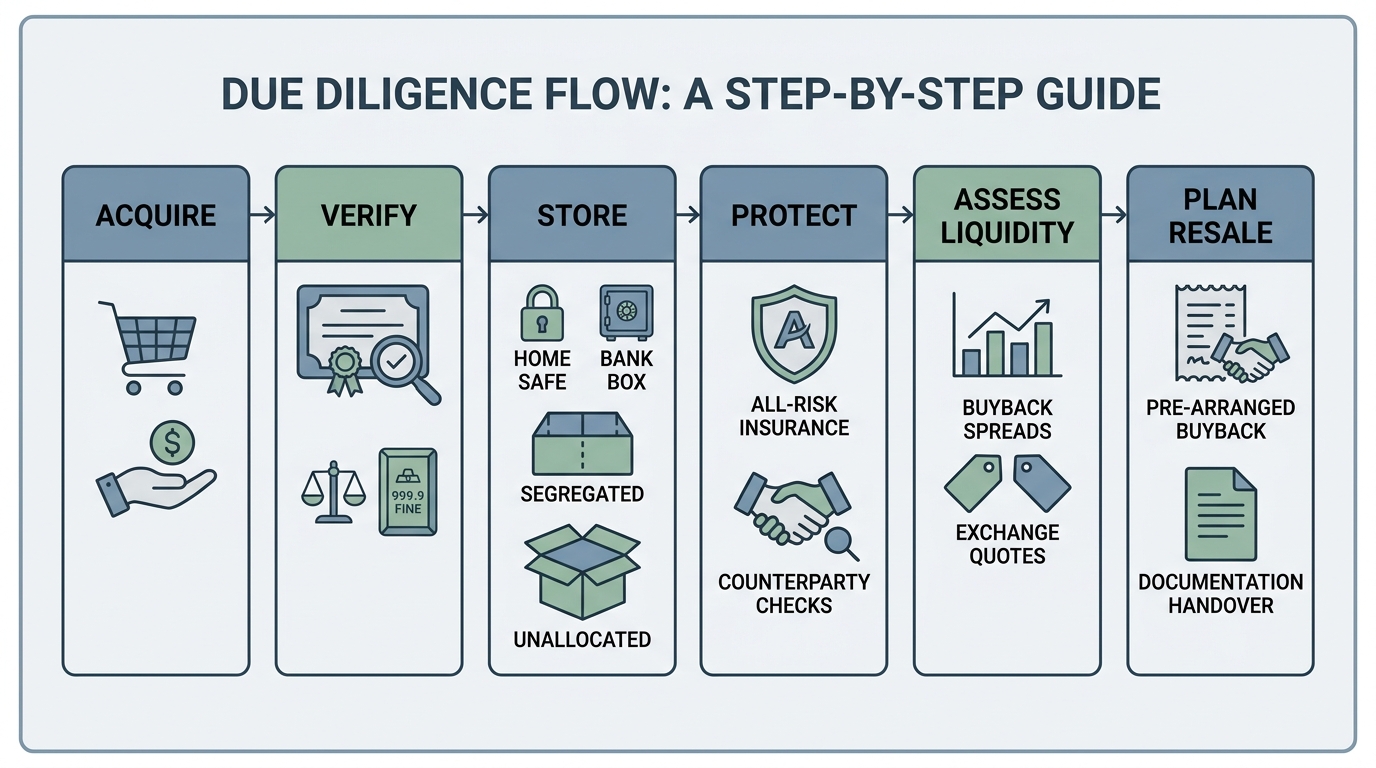

3. Implementation Roadmap

The practical sequence is straightforward: define what you will buy, verify what arrives, place it in the right custody model, protect it with insurance and controls, and confirm that liquidity works before you need it.

Phase 1: Source Only What You Can Defend Later

Approve dealer and refiner criteria. For bullion, favor LBMA-accredited or equivalent refiners where relevant. Review dealer reputation, operating history, complaint patterns, and buyback terms.

Demand transparent pricing. The quote should clearly separate spot price, premium, shipping, storage setup, and any handling fee.

Select practical unit sizes. For gold and silver, 1 oz to 100g bars often support both value density and resale ease. Larger bars can work for family offices or institutional mandates, but exit flexibility may be narrower.

Match form to purpose. Coins and smaller bars may improve flexibility; kilobars and larger bars can suit larger allocations; industrial lots must match end-use or market-accepted specifications.

Leadership decision: Approve a purchase universe before buying. That usually includes approved metals, refiners, sizes, and jurisdictions. It prevents ad hoc buying that later creates storage or resale friction.

Phase 2: Verify Purity, Provenance, and Packaging

Confirm fineness standards. Bullion buyers commonly expect gold and silver at bullion-grade purity levels, ideally very high fineness; platinum and palladium are typically held to similarly strict standards. For nickel, cobalt, or specialty alloys, the relevant question is whether the material meets the resale or manufacturing specification.

Require hallmarks and serial numbers. The product should show a clear refiner mark, weight, stated purity, and a unique serial number where applicable.

Inspect packaging integrity. Original tamper-evident packaging can strengthen resale confidence, especially for retail-format bullion.

Use independent testing when appropriate. XRF analysis, assay, or accredited lab testing may be appropriate for non-standard material, secondary market inventory, or industrial grades.

Retain a full evidence file. Keep invoices, assay certificates, product photos, packing slips, bar lists, and transport records. A retention period of at least seven years is a practical minimum in many organizations.

Leadership decision: Set a rule that no asset enters the long-term inventory without a complete provenance file. In physical markets, documentation is not paperwork overhead; it is part of the resale value.

What This Means for You: A metal position with weak records may still be genuine, but it can become slower and more expensive to finance, transfer, or liquidate.

Phase 3: Design the Right Storage and Custody Model

Physical strategic metals storage should be selected based on asset value, access needs, jurisdictional considerations, and the importance of direct title. For most executive programs, the real choice is not “where can we put it,” but “what storage model best preserves ownership certainty and saleability.”

On-site or home storage: suitable only for modest holdings or emergency-access requirements. It raises concentration, security, and insurance concerns.

Bank safe deposit boxes: can provide familiar custody, but access windows, insurance arrangements, and audit practicality may be limited.

Professional segregated vaulting: usually the strongest institutional choice for high-value holdings because specific bars or lots are identified as yours.

Unallocated or commingled storage: may lower fees and simplify trading, but it introduces more counterparty dependence because title is less direct.

Confirm ownership structure. Ask whether the arrangement is allocated, segregated, or unallocated, and verify how title is documented.

Check audit rights. Independent third-party audits, reconciled bar lists, and exception reporting should be standard.

Review withdrawal terms. Understand notice periods, minimum withdrawal sizes, transport procedures, and associated fees.

Assess environmental controls. Silver and industrial materials may be more sensitive to moisture, packaging damage, or contamination than investors initially expect.

Choose politically and legally stable jurisdictions. Jurisdiction selection affects enforceability, transport, taxation, and recovery options in disputes.

Leadership decision: For material holdings, segregated and insured vaulting in a stable jurisdiction is often worth the additional cost because it improves auditability, counterparty protection, and resale confidence.

End-to-end strategic metals due diligence checklist flow.

Illustrative 90-Day Timeline

Days 1-15: define mandate, metal types, approved sizes, budget, and governance owners.

Days 16-30: shortlist dealers, refiners, vaults, insurers, and any assay partners; review legal and tax implications.

Days 31-60: complete onboarding, open custody accounts, document verification standards, and finalize reporting templates.

Days 61-75: execute first purchase, verify delivery records, and reconcile bar lists or lot details.

Days 76-90: test reporting, audit reconciliation, and if feasible, a small withdrawal or buyback process.

What This Means for You: A short implementation timeline is possible, but only if governance, documentation standards, and partner selection are established before the first purchase order is issued.

Phase 4: Protect the Asset with Insurance and Counterparty Controls

Verify all-risk coverage. Confirm what is covered during storage, transit, and handling, and review exclusions carefully.

Assess provider strength. The vault operator, insurer, and logistics provider should all be financially credible and operationally mature.

Diversify where appropriate. A single provider or single jurisdiction may be efficient, but it also concentrates operational and political risk.

Reconcile statements regularly. Monthly or quarterly inventory reconciliation should be part of the operating cadence.

Screen for compliance issues. Cross-border movement may trigger sanctions checks, customs rules, tax treatment, or origin-related compliance review.

Leadership decision: Insurance should be reviewed as a board-level or investment-committee control for material holdings, not as a routine back-office detail.

Phase 5: Build the Resale Path Before You Need It

Liquidity is often misunderstood. A metal may be valuable, but that does not mean it can be sold quickly, locally, or at a tight spread. The likely exit path should shape the original purchase decision.

Map likely buyers in advance. Gold and silver generally have broad markets; platinum and palladium can be narrower; industrial strategic metals may require specialized counterparties or end-users.

Review buyback terms before purchase. A good partner can explain spread methodology, settlement timing, and any conditions tied to packaging or storage chain-of-custody.

Preserve resale-friendly condition. Intact packaging, serial verification, and continuous custody can reduce questions at sale.

Test the process. A small partial sale or transfer can reveal practical delays before a larger exit is necessary.

Understand local constraints. Tax, VAT or GST treatment, import rules, and dealer documentation requirements vary by jurisdiction.

Leadership decision: If liquidity is a priority, avoid buying forms that only a small number of counterparties will accept. The narrower the market, the more important documentation and specification become.

What This Means for You: In strategic metals due diligence, the best time to plan the sale is before the purchase. Exit friction is much easier to prevent than to fix.

4. Risk Mitigation

Opaque dealer pricing: mitigate by requiring line-item quotes showing spot, premium, and every fee.

Counterfeit or misdescribed material: mitigate by buying from recognized sources, checking hallmarks and serials, and using independent assay where warranted.

Wrong bar or lot size: mitigate by aligning unit size with intended resale channel and position size.

Weak title or custody language: mitigate by documenting whether holdings are segregated, allocated, or unallocated and by confirming beneficial ownership.

Inadequate insurance: mitigate through documented all-risk coverage, periodic policy review, and alignment with current inventory value.

Single-point failure: mitigate through provider, location, or jurisdiction diversification when exposure becomes material.

Documentation gaps: mitigate with a mandatory file standard and a retention policy of seven years or longer where appropriate.

Resale surprises: mitigate through pre-arranged buyback discussions and at least one test transfer or liquidation.

What This Means for You: Most losses in physical metal programs come from operational weaknesses, not from the metal itself. Governance is the real hedge.

Purity and authenticity verification workflow (illustrative).

5. Success Indicators

Executives should track a short set of measurable indicators that show whether the program remains controlled, liquid, and policy-compliant.

Provenance completeness: percentage of holdings with invoices, certificates, serial records, and storage confirmation.

Policy compliance: percentage of holdings sourced from approved refiners, dealers, and jurisdictions.

Storage quality: percentage stored in segregated or otherwise policy-approved custody.

Insurance adequacy: insured value compared with current replacement value and transport exposure.

Audit performance: number of exceptions found in independent reconciliations.

Liquidity performance: time required to transfer or liquidate a test lot under normal conditions.

Total carrying cost: annualized cost of storage, insurance, verification, and administration as a share of asset value.

Concentration risk: share of holdings exposed to one provider or one jurisdiction.

What This Means for You: If management reporting only shows the metal price and not the custody, audit, insurance, and liquidity metrics above, leaders are not seeing the full risk picture.

6. Partner Selection

The right implementation support can reduce both operational risk and decision fatigue. The goal is not to outsource accountability, but to choose partners whose processes make oversight easier.

Dealers and refiners: look for recognized accreditation where relevant, transparent pricing, published buyback practices, and a clear escalation path for disputes.

Vault and custody providers: prioritize clear title structures, independent audits, robust physical security, detailed reporting, and credible insurance arrangements.

Assay and testing partners: use accredited laboratories or accepted testing providers when non-standard or industrial materials require verification.

Logistics partners: require secure transport, documented chain-of-custody, and experience with cross-border compliance.

Advisory support: legal, tax, and compliance partners should be comfortable with global metal ownership, storage jurisdiction issues, and resale documentation.

Red flags to avoid: pressure selling, unclear ownership language, vague insurance answers, resistance to third-party audit, no transparent buyback method, and poor documentation discipline.

What This Means for You: Good partners reduce friction at every stage, but the strongest signal of quality is not marketing language. It is the consistency of their records, contracts, controls, and willingness to support verification.

Final Takeaway

A disciplined approach to physical strategic metals storage turns a simple purchase into a resilient ownership program. For executive teams, the checklist is clear: buy recognized material, verify purity and provenance, store it under a custody model that preserves title, insure it properly, measure liquidity before it is needed, and select partners that make auditability easy. That is the foundation of effective metal storage and sound strategic metals due diligence in a global market.

**Magnet metals are no longer a niche materials topic. They sit at the center of EV efficiency, wind turbine reliability, and defense readiness. This explainer breaks down what NdPr, dysprosium, and terbium actually do inside rare earth magnets, where the real supply-chain bottlenecks sit, why substitution remains difficult, and what practical sourcing strategies reduce cost and risk.**

Neodymium, Praseodymium and Dysprosium: The Magnet Metals Behind EVs, Wind Power and Defense

For industrial buyers, engineers, supply-chain analysts, and investors, magnet metals are not an abstract commodities story. They directly shape motor size, generator efficiency, thermal performance, lead times, and margin stability. In electric vehicles, offshore wind, aerospace, robotics, and defense systems, the same issue keeps surfacing: how do you secure high performance without locking your business into avoidable supply risk?

Traditional approaches still exist. Ferrite magnets are cheaper. Induction and switched reluctance motor designs can reduce or avoid rare earth dependence. Gear-driven wind systems can limit magnet use. But old approaches often fall short where compact size, low weight, low maintenance, and high efficiency matter most. This means for your business: the real cost is not just the metal price. It is redesign, extra cooling, larger housings, more maintenance, and delayed programs when material strategy is treated as an afterthought.

[BUSINESS_IMPACT] Typical Results: Higher power density in compact motors | Better high-temperature reliability | Lower maintenance in direct-drive systems Implementation Time: 6 to 18 months for redesign, qualification, and supplier approval ROI Timeline: 12 to 36 months, depending on application and procurement strategy [/BUSINESS_IMPACT]

Why rare earth magnets outperform older solutions

The reason magnet metals matter is simple: neodymium-iron-boron magnets, commonly called NdFeB magnets, deliver exceptional magnetic strength in a small package. That allows engineers to build motors and generators that are lighter, more compact, and more efficient than many alternatives. In EVs, that can mean better torque density and improved efficiency across real driving cycles. In wind power, it enables direct-drive generators that remove gearbox complexity. In defense, it supports compact actuators, precision guidance, radar subsystems, and electric drive components where size and reliability are critical.

Companies like yours typically see the biggest benefit when space, heat, and uptime are constrained at the same time. A magnet decision is rarely just a materials decision. It affects thermal design, power electronics, enclosure size, maintenance intervals, and even shipping weight. Here’s what actually moves the needle: understanding which metal provides core magnetic force, and which metals act as thermal insurance.

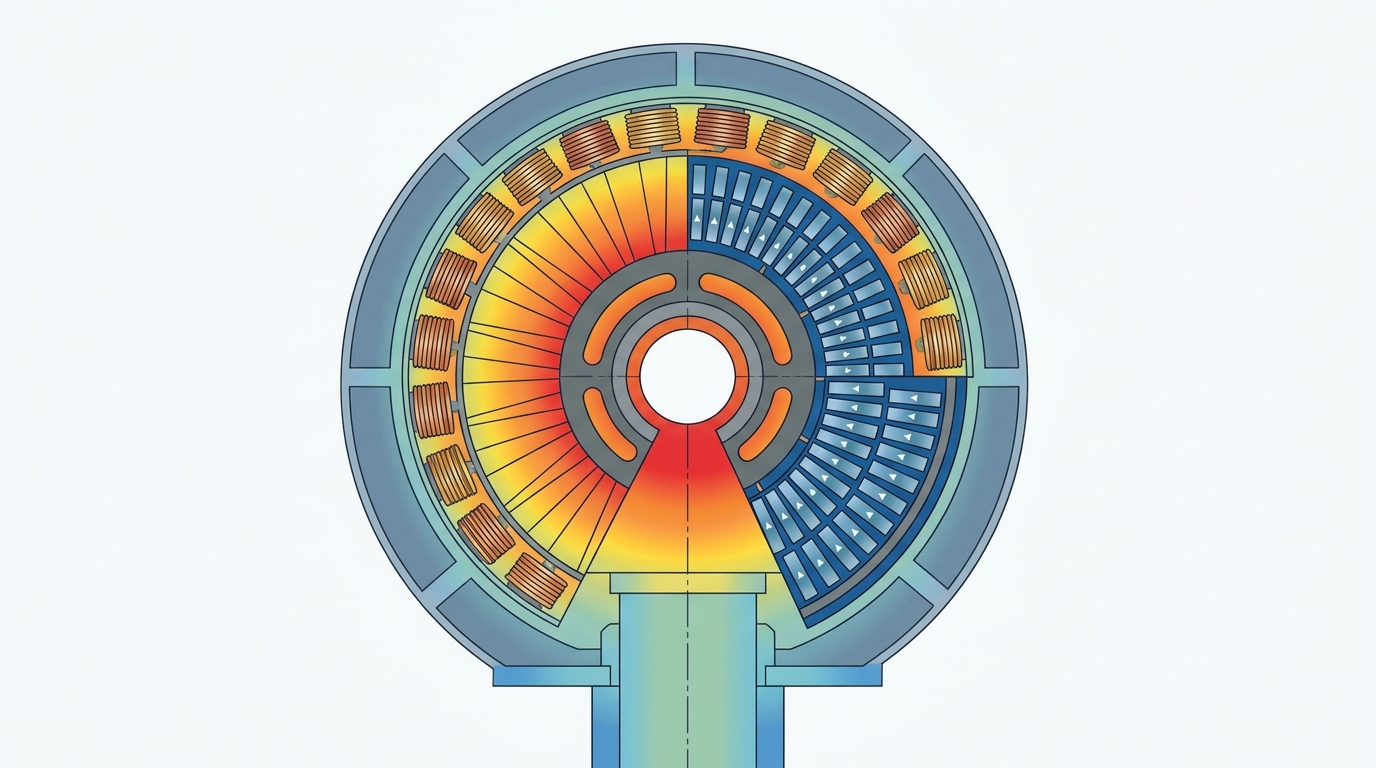

What NdPr, dysprosium, and terbium actually do

NdPr is industry shorthand for neodymium plus praseodymium. These two light rare earth elements are often discussed and traded together because they sit close together in the refining chain and because both contribute to the magnetic performance of NdFeB magnets. Think of NdPr as the core ingredient that gives the magnet its strength. It provides the high magnetic flux that makes permanent magnet motors small and powerful.

Dysprosium and terbium play a different role. They are used in smaller amounts to improve coercivity, which is the magnet’s resistance to losing magnetism under heat and stress. In plain terms, NdPr gives you the muscle; dysprosium and terbium help that muscle keep working when temperatures rise. This is especially important in EV traction motors, high-duty industrial drives, offshore wind generators, and defense systems exposed to harsh operating conditions.

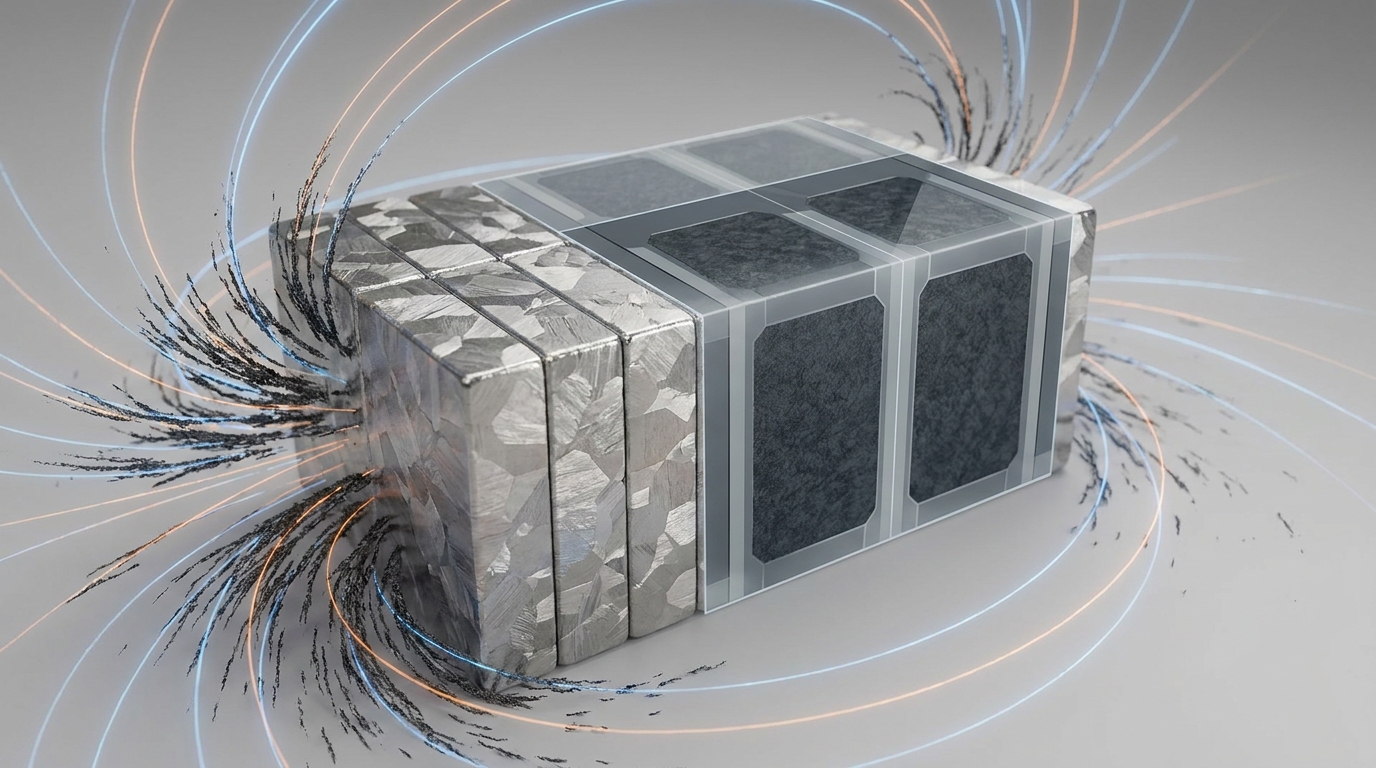

Visualizing how NdFeB rare-earth magnets use NdPr as the main magnetic phase and Dy for high-temperature coercivity.

Neodymium: Delivers most of the base magnetic strength in NdFeB magnets.

Praseodymium: Works alongside neodymium in the magnetic structure and is commonly part of the commercial NdPr mix.

Dysprosium: Raises heat resistance and helps magnets hold performance at elevated temperatures.

Terbium: Also improves high-temperature coercivity, often even more effectively than dysprosium, but it is scarcer and typically more expensive.

One important nuance for buyers and engineers: more dysprosium or terbium is not always better. Heavy rare earth additions improve thermal stability, but they can also reduce peak magnetic performance and raise cost sharply. That is why the right question is not, “How much Dy or Tb can we add?” It is, “What is the minimum heavy rare earth content needed to meet the real operating temperature?”

Where magnet metals sit in the global value chain

The magnet metals supply chain is more complicated than many procurement teams first expect. Mining is only the starting point. Ore must be processed into separated rare earth oxides, then converted into metals or alloys, then turned into magnet powder, sintered or bonded into finished magnets, machined, coated, and finally integrated into motors or generators. The biggest business lesson is this: mining diversification alone does not solve supply risk if separation, alloying, and magnet manufacturing remain concentrated.

Upstream: Mining and concentrate production from rare earth-bearing ores.

Midstream: Separation, refining, metal making, and alloy production.

Downstream: Magnet manufacturing, motor or generator assembly, and system integration.

Globally, the most serious choke points are still in the midstream and magnet-making stages. China remains the dominant force in separation and finished magnet production, while heavy rare earth supply for dysprosium and terbium is even narrower. For investors, this means the most strategic bottlenecks are often not the mine itself but the refining and fabrication capabilities that convert ore into usable magnetic material.

Why substitution is harder than it sounds

On paper, substitution sounds attractive. Use ferrite magnets. Shift to induction motors. Move to switched reluctance designs. Reduce or eliminate heavy rare earth content. In practice, each option changes the rest of the system. Ferrite magnets are far weaker, so motors typically get larger and heavier. Rare-earth-free motor designs often need more sophisticated controls, different torque characteristics, or changes in cooling and acoustics. In wind power, alternative drivetrain choices can bring back maintenance trade-offs that permanent-magnet direct-drive systems were designed to remove.

Explaining why dysprosium-stabilized NdFeB magnets help maintain generator performance under offshore temperature extremes.

There are real improvements happening. Grain-boundary diffusion and other magnet engineering techniques can reduce dysprosium usage while preserving heat resistance. Better cooling can allow lower-Dy designs in some EV and industrial applications. But these are optimization strategies, not complete escape routes. What we see across the market is that substitution usually shifts cost elsewhere rather than making it disappear.

Ferrite magnets: Lower cost and more abundant, but much lower magnetic strength.

Induction or switched reluctance motors: Can reduce rare earth exposure, but may require larger systems or more complex control strategies.

Low-Dy designs with added cooling: Lower material intensity, but potentially higher thermal-system cost and tighter operating limits.

Dy-saving magnet processes: Useful for reducing heavy rare earth loadings, but they do not eliminate NdPr dependence.

For engineers, the key trade-off is usually temperature. If the application runs hot, heavy rare earths may still be the most practical answer. For supply-chain teams, the key trade-off is qualification time. Even when a substitute exists, validating a new motor architecture or magnet grade can take far longer than a buyer wants during a supply squeeze.

The supply-chain risks that matter most

There are four risks that deserve board-level attention. First is concentration risk: too much of the world’s separation and magnet production sits in a small number of geographies. Second is heavy rare earth scarcity: dysprosium and terbium are used in smaller quantities than NdPr, but their supply is tighter and more vulnerable to disruption. Third is demand acceleration: EVs, wind power, automation, and defense are all pulling on the same material pool. Fourth is qualification risk: a magnet shortage is not solved quickly if your approved supplier list is too short.

In our experience with similar companies, the most expensive mistake is treating rare earth magnets as a standard catalog buy. Price charts alone do not tell the full story because oxide, metal, alloy, and finished magnet markets can move differently. Lead times can also widen at the alloy or sintering stage even when upstream material looks available. That is why a sourcing plan must map the whole chain, not just the mine origin.

[KEY_CONSIDERATIONS] ✓ High-performance rare earth magnets can unlock system efficiency, compact design, and lower maintenance ✓ Dual-sourcing and longer-term contracts reduce exposure to sudden price spikes and allocation risk ⚠ Over-specifying dysprosium or terbium can inflate cost and reduce magnetic performance if the heat margin is not actually needed [/KEY_CONSIDERATIONS]

Illustrating the reliability role of rare-earth magnets in extreme-condition defense electrics.

What actually moves the needle for buyers, engineers, and investors

A practical procurement strategy starts with separating must-have performance from nice-to-have margin. Engineers should define the true thermal window, duty cycle, corrosion exposure, and service life. Buyers should then source to that specification, not to a blanket “highest grade available” rule. This is where the biggest savings often appear. The difference between a high-dysprosium magnet and a lower-Dy design with improved cooling can materially change cost, availability, and redesign complexity.

Spec selection: Use high-Dy grades when the application genuinely needs heat resistance; use lower-Dy grades only when cooling, duty cycle, and reliability targets clearly support the trade-off.

Contract structure: Lock roughly 70% of forecast volume under 3-year agreements and keep the remaining portion flexible for spot or opportunistic buying.

Risk mitigation: Dual-source NdPr and dysprosium where possible, and qualify alternative magnet makers before a disruption hits.

Recycling strategy: Allocate around 5% of the relevant materials or innovation budget to recycling pilots and magnet recovery partnerships.

Design alignment: Bring procurement, engineering, and program management into the same review process so material choices and thermal design are made together.

For investors, the message is equally clear. The most resilient companies are not simply the ones with exposure to rare earth demand growth. They are the ones that control bottlenecks, qualify more than one route to supply, and invest in recycling or alloy optimization before the market tightens. Margin durability will increasingly come from supply-chain design, not just end-market growth.

Where the real impact shows up in EVs, wind power, and defense

In EVs, rare earth magnets enable compact traction motors with strong torque density and high efficiency. That can translate into smaller packages, less battery draw for the same drive cycle, or more performance from the same vehicle platform. In wind power, permanent-magnet direct-drive systems reduce gearbox dependence and can improve maintenance economics, especially offshore where every service trip is expensive. A single large turbine can contain significant magnet volumes, so grade decisions matter both technically and financially. In defense, the volumes may be smaller than automotive, but qualification, reliability, and security-of-supply requirements are much stricter.

The common thread is that these are high-consequence applications. When performance matters, substitution is rarely a simple one-for-one swap. The choice is usually between paying more for the right magnetic chemistry now or paying later through redesign, reduced efficiency, or program delay.

Your path forward

Map every component in your portfolio that depends on rare earth magnets.

Separate applications by thermal severity, duty cycle, and uptime criticality.

Define approved high-Dy, low-Dy, and diffusion-enhanced grades where relevant.

Secure base-load volume with multi-year contracts and dual-source critical materials.

Start small but real recycling and recovery programs now, before they become urgent.

Track cost, lead time, temperature margin, and recycled content as part of the same KPI set.

Magnet metals will remain strategically important because they solve a very practical business problem: how to get more performance from less space, less weight, and less maintenance. Neodymium and praseodymium provide the core magnetic strength. Dysprosium and terbium provide thermal resilience. The companies that win will be the ones that treat those facts as part of product strategy, not just raw-material purchasing. That is how you turn a critical-minerals risk into an operational advantage.