Breaks in the physical strategic metals chain rarely begin with a dramatic mine shutdown. In day-to-day reviews, disruption more often appears as a missing lot number on a warehouse receipt, an assay that cannot be tied to the exact drums in storage, a provenance file that stops at the trader rather than the processor, or a resale inquiry that stalls because the material form is not widely accepted. That is the operating context for physical strategic metals due diligence: a document-heavy, lot-specific review used by family offices, private wealth advisers, and physical commodity buyers dealing with materials that sit outside standardized exchange inventories.

- Key takeaway 1: Purity alone rarely closes the file; the decisive question is whether purity data can be tied to a named lot through sealed sampling, dated assays, and a clean title chain.

- Key takeaway 2: Strategic metals custody and storage risk often sit in the gap between warehouse paperwork and legal title, especially in pooled arrangements or free-zone transfers.

- Key takeaway 3: Resale friction usually comes from non-standard form, stale assay data, missing provenance, or a narrow buyer universe rather than from the metal name itself.

- Key takeaway 4: Fees and handling charges matter less as headline numbers than as signals of who controls withdrawal, re-assay, relabeling, and final release of the lot.

The review perimeter: product form, lot identity, and marketability

A workable strategic metals checklist usually begins with the physical reality of the product. The same element can trade as oxide, metal, alloy, carbonate, sulfate, powder, or briquette, and those forms do not travel through the same buyer network. Rare earth materials often use TREO, or total rare earth oxide, as a headline measure, while lithium volumes are sometimes compared on an LCE, or lithium carbonate equivalent, basis even when the stored material is a specific salt. Impurities may be recorded in percent or in ppm, parts per million, and small differences at that level can separate an acceptable industrial lot from a restricted one.

One recurring discovery in market reviews is that commercial descriptions sound standardized while the underlying product is not. “Neodymium-praseodymium oxide” may be chemically close to expectation but packaged in unsealed fiber drums, or “nickel units” may describe a form that lacks broad acceptance in downstream processing. Another common gap appears when origin, processing jurisdiction, and current storage location sit in three different countries. Chinese-origin rare earth oxide routed through a third-country processor is a typical example where paper continuity matters as much as chemistry.

Purity and metal purity documentation

The core evidence set for purity normally includes a recent Certificate of Analysis, the analytical method, the sample chain, and the lot identifier. In observed market practice, stronger files contain an assay from an ISO/IEC 17025-accredited laboratory such as SGS, Bureau Veritas, or Alex Stewart International. For rare earth elements, ICP-MS – Inductively Coupled Plasma Mass Spectrometry – is commonly used where trace impurities matter. For base metals such as nickel, XRF, or X-ray fluorescence, is often part of the package, though its usefulness depends on the material form and the impurity profile being tested.

- A dated Certificate of Analysis linked to a specific lot or container number

- Sampling records showing sealed transfer, tamper evidence, and sampler identity

- Impurity breakdown rather than headline purity alone, including radioactive or deleterious elements where relevant

- Assay age, with files older than six months often treated in the market as weaker evidence for active resale or transfer

- Dual-assay files where one result comes from a seller-linked lab and one from an independent laboratory

A well-known failure mode is the seller-lab assay that looks complete but does not describe how the sample was taken from the physical lot. That gap is especially visible in some Chinese-sourced lots, where the chemistry appears attractive until an independent re-assay ties the result to the actual drums or bags. In practice, a variance above 0.5% between the seller assay and the independent assay often shifts a lot into dispute or further sampling. Another discovery that changes downstream usability is impurity content that was not emphasized in the first document pack. A 2024 market example involving praseodymium oxide centered on re-assay findings of 2% thorium impurities, illustrating how a lot can move from apparently acceptable to operationally restricted.

Provenance, traceability, and compliance exposure

Purity answers only part of the question. Provenance asks where the material was mined, processed, refined, exported, stored, and transferred, and whether those steps align with current compliance screens. The latest change in many reviews is that documentary sufficiency now extends beyond a Certificate of Analysis into sanctions checks, forced-labour exposure, and named processing entities. In practical terms, the stronger provenance file follows the lot from mine or processor through export documents and into storage, rather than stopping at a trading company invoice.

- Commercial invoice, packing list, and transport document tied to the same lot reference

- Processor or refiner statement identifying where transformation occurred

- Customs or free-zone documentation showing entry, transfer, and current location

- Sanctions and forced-labour screening records for relevant jurisdictions, including U.S. and EU exposure

- OECD-aligned traceability reports or, in some cases, blockchain-linked certificates as supplementary evidence

Failure modes in this section tend to be structural rather than clerical. The mine origin may be named but the processing plant omitted. The exporter may be visible while the beneficial owner of the intermediary remains unclear. Corporate restructurings can also break the chain when an old entity name appears on the assay and a newer name appears on the shipping file. Those mismatches become more sensitive where transshipment, China-linked processing, Myanmar border material, or Russia-related restrictions enter the record.

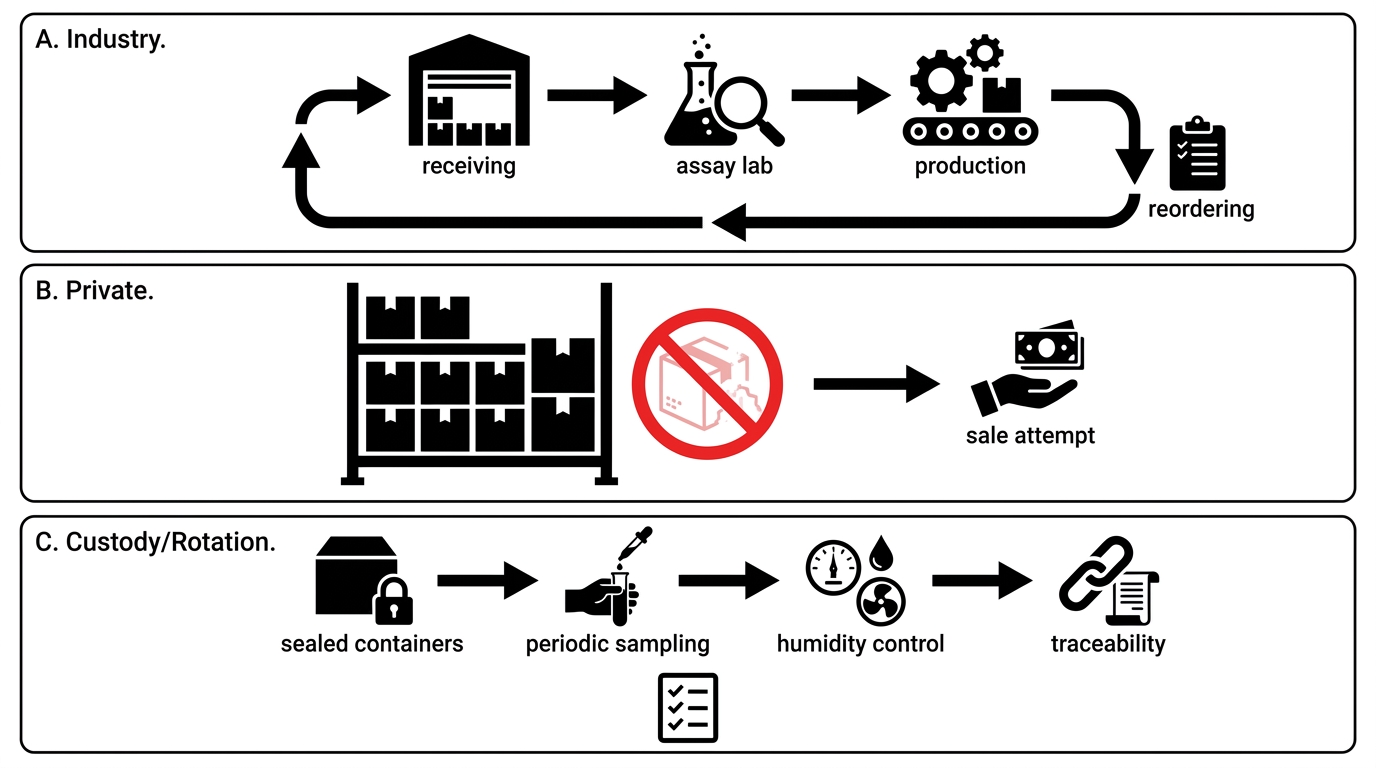

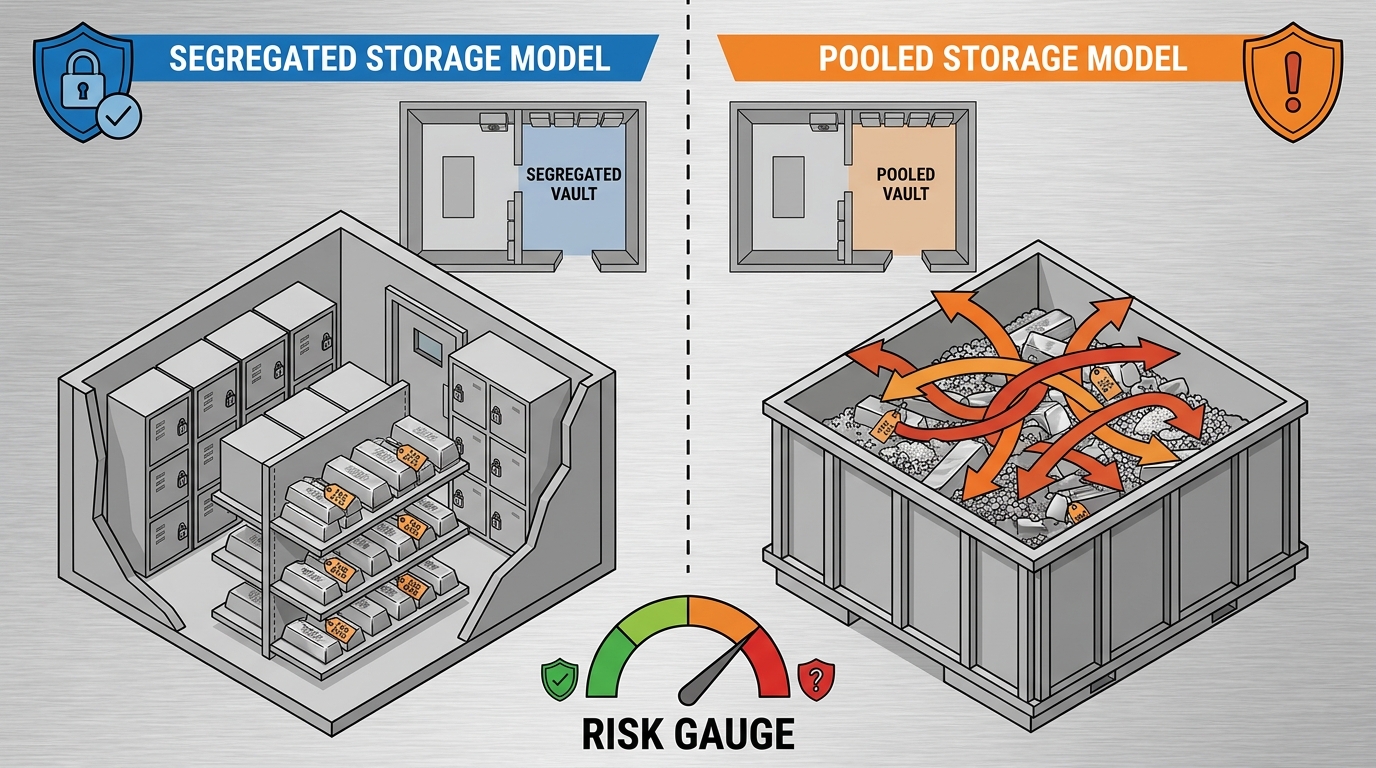

Strategic metals custody and physical strategic metals storage

Strategic metals custody differs from precious-metals storage because lot-specific form and downstream usability often matter more than fungibility. A segregated arrangement generally preserves a named lot, original packaging state, and cleaner re-assay path. A pooled arrangement can work for more standardized units, but it introduces uncertainty if a later buyer wants the original provenance pack, exact drum numbers, or a fresh sample from the same material that entered storage. In other words, storage design directly affects resale readiness.

- Segregated storage: clearer title, cleaner audit trail, easier reconciliation between assay, packaging, and inventory record

- Pooled storage: simpler administration in some cases, but weaker lot continuity and more difficult recovery of original evidence

- Jurisdiction: Singapore, Switzerland, and the United States appear frequently in reviews because legal enforceability and customs handling are easier to map

- Condition of goods: sealed inner liners, moisture exposure, damaged drums, relabeling, and repacking history all affect claim quality

A common moment of discovery appears when the warehouse receipt confirms weight and location but not the full lot identity. Another appears when the storage invoice looks institutional while the legal title still sits with an affiliate of the seller. For powders, salts, and reactive materials, storage specifications can become decisive: hazardous classification, humidity control, fire protection, and access logs may determine whether the material remains insurable and transferable in the same form in which it arrived.

Insurance, title chain, and documentation hygiene

Insurance analysis in this market is less about generic coverage language and more about alignment between the insured party, the named custodian, the storage site, and the lot description. The title chain sits at the center of that review. If the seller, transporter, warehouse operator, and insured entity do not line up across the file, recovery rights become harder to interpret. This is one reason documentation hygiene carries so much weight in physical strategic metals transactions.

- Warehouse receipt or inventory certificate that identifies the lot with specificity

- Insurance binder or certificate showing covered location, peril scope, and named insured

- Title transfer records from seller to current owner, including any free-zone or bonded transfer

- Audit or inventory reconciliation reports from the custodian

- Incident procedures for contamination, damage, partial loss, or assay dispute

Observed weak points include blanket insurance policies with unclear sub-limits, inventory reports issued by a storage affiliate rather than the actual operator, and files that cover theft but say very little about contamination, degradation, or disputed purity. In practice, those issues do not always surface at purchase; they emerge when the lot moves, when a buyer requests a fresh assay, or when packaging damage forces repacking and changes the original evidence trail.

Liquidity, resale constraints, and counterparty risk

Physical strategic metals become hard to resell for predictable reasons: the buyer pool is narrow, the product form is non-standard, the assay is stale, the provenance file is incomplete, or the material sits in a jurisdiction that complicates release. Liquidity also varies sharply by product. A recognizable NdPr oxide lot with current assay data and clear custody records tends to be easier to place than an obscure minor metal, a mixed intermediate, or an off-spec blend. Counterparty analysis therefore extends beyond financial standing into operational history, dispute record, and document discipline.

- Evidence of prior two-way market activity for the same form and specification

- Named counterparties willing to review fresh assay data and original provenance records

- Clear schedules for storage, handling, withdrawal, re-assay, and relabeling, since these often reveal where control actually sits

- Consistency between legal entity names on invoices, assays, insurance records, and warehouse reports

The practical lesson from this section is simple: resale friction is often a documentation problem disguised as a market problem. A buyer may like the chemistry but pause because the assay predates transfer, or because the intermediary changed name after shipment, or because the warehouse cannot confirm that the drums offered for release are the same drums sampled for the original Certificate of Analysis.

Closing frame

As a working framework, this strategic metals checklist turns a broad risk question into a series of verifiable files: product form, lot identity, assay quality, provenance continuity, custody model, storage jurisdiction, insurance scope, title chain, and resale readiness. The most consistent pattern across all categories is that a lot becomes easier to evaluate when the chemistry, the documents, and the physical storage record describe the same thing in the same sequence. Related reading in the Procyon Metals library includes the critical metals pillar guide and the rare earth magnets supply chain guide.

Procyon Metals maintains a working due diligence checklist for teams reviewing physical strategic metals and is available to discuss custody and sourcing questions in a factual scoping conversation.